Q3 Operational Update Commentary

Operationally the company met or exceeded every projection from the Q2'06 C.C. with only one exception. The lone exception was a projection of 6 development wells on Seven Rivers Queen to be drilled in Q3. There were actually 2 wells drilled on this property. In order to meet the total wells drilled projection for Q3 the company drilled 3 extra wells on the Fuhrman-Mascho property, 1 extra well on the Eva South property in OK, and 1 extra well on the Ona Morrow property in OK. (Keep in mind that if one added up all the individual wells to be drilled by property as projected in the Q2'06 C.C. the total would come out to 35. However, the company projected 36 total wells at that time allowing for one additional well to be drilled somewhere.)

ARD Incremental Oil and Gas Production

The quarter over quarter growth in total oil and gas produced was very impressive. The incremental increase produced (Q3 over Q2) was about 53,940 BOE (295,000 to 241,060 BOE.) The previous quarter (Q2) saw a quarterly incremental increase of 50,271 BOE (241,060 to 190,789.) On an absolute basis the change in incremental oil and gas production between Q3 and Q2 when compared to Q2 and Q1 increased 3669 BOE. This translates into a 7.2% increase in absolute incremental production in the Q3-Q2 period over the Q2-Q1 period. Considering that this increase occurred in the face of the natural declines in the ever expanding inventory of wells says a lot. To be clear, it means that the 295,000 BOE produced was very impressive.

We should realize about 85% of total production being oil. This is down slightly from the 86.2% reported in Q2. Given the fact that NG prices are so depressed and given the fact that the vast majority of domestic E&P companies have well under 50% of total production being oil, one should expect Arena Resources to command an earnings multiple premium to other oil and gas producers.

Benchmarking ARD with 2 Other Companies

Currently ARD shares command significant value based on the fact that comparisons to other companies with larger market caps (slower growth prospects) and/or higher percent production being NG reveal that the other companies in the comparison have a higher earnings multiple than ARD. In other words 2 other companies that are fundamentally inferior with slower growth prospects have an unjustified earnings multiple premium when compared to ARD.

For example UPL is growing production, revenues, net income and EPS slower than ARD (ARD has the better future prospects.) UPL also has a higher percent of production in NG. Currently the market is giving UPL an earnings multiple of 29 in comparison to the ARD earnings multiple of 28.

One other example of the ARD earnings multiple being lower than another company that produces a significantly lesser amount of oil as a percentage of total production is GMXR. GMXR has less than 10% production in oil. Also GMXR growth in production, revenues, net income and EPS is much slower than ARD. (ARD has the better future prospects.) Currently the market is giving GMXR an earnings multiple of 38 in comparison to the ARD earnings multiple of 28.

Since ARD will grow earnings faster than both UPL and GMXR we can also conclude that ARD currently has a lower foward PE than both UPL and GMXR.

Expect that ARD earnings multiple to continue to expand back into the mid 30's or higher.

What can we expect for Q3'06 earnings?

Revenues: $17.9 million........ (up from $14.69 mm in Q2'06)

Net Profit Margin: 42%......... (down from 43.8% in Q2'06.)

Net Income: $7.51 million.....(up from $6.44 mm in Q2'06.)

Share Count*: 15 million.......(up from 14.64mm in Q2'06.)

*(Fully diluted)

EPS: $0.50.......(Up from $0.44 in Q2'06/ $0.27 in Q3'05.)

The projected quarter over quarter decline in net profit margin is a result of the potential for "other expenses" increasing due to NYSE listing fee requirements of at most $150,000. We'll have to wait and see how much of the listing fees are expensed in the third quarter. In terms of EPS this ($150,000) amounts to one penny ($0.01.)

Ttm Earnings will increase to $1.40. Put a earnings multiple of 29 on these earnings and you have a share price of $40.60. A more realistic multiple would be 35. This would yield a share price of $49. (One Wall Street firm recently put a target price on ARD shares of $49.)

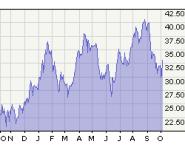

The 1 year chart below indicates that ARD has been making higher lows and higher highs.

ARD 1 Year Price Chart

Expect the trend to continue as ARD earnings per share increase over time. The three most important drivers of share price appreciation are earnings, earnings, earnings.

Operationally the company met or exceeded every projection from the Q2'06 C.C. with only one exception. The lone exception was a projection of 6 development wells on Seven Rivers Queen to be drilled in Q3. There were actually 2 wells drilled on this property. In order to meet the total wells drilled projection for Q3 the company drilled 3 extra wells on the Fuhrman-Mascho property, 1 extra well on the Eva South property in OK, and 1 extra well on the Ona Morrow property in OK. (Keep in mind that if one added up all the individual wells to be drilled by property as projected in the Q2'06 C.C. the total would come out to 35. However, the company projected 36 total wells at that time allowing for one additional well to be drilled somewhere.)

ARD Incremental Oil and Gas Production

The quarter over quarter growth in total oil and gas produced was very impressive. The incremental increase produced (Q3 over Q2) was about 53,940 BOE (295,000 to 241,060 BOE.) The previous quarter (Q2) saw a quarterly incremental increase of 50,271 BOE (241,060 to 190,789.) On an absolute basis the change in incremental oil and gas production between Q3 and Q2 when compared to Q2 and Q1 increased 3669 BOE. This translates into a 7.2% increase in absolute incremental production in the Q3-Q2 period over the Q2-Q1 period. Considering that this increase occurred in the face of the natural declines in the ever expanding inventory of wells says a lot. To be clear, it means that the 295,000 BOE produced was very impressive.

We should realize about 85% of total production being oil. This is down slightly from the 86.2% reported in Q2. Given the fact that NG prices are so depressed and given the fact that the vast majority of domestic E&P companies have well under 50% of total production being oil, one should expect Arena Resources to command an earnings multiple premium to other oil and gas producers.

Benchmarking ARD with 2 Other Companies

Currently ARD shares command significant value based on the fact that comparisons to other companies with larger market caps (slower growth prospects) and/or higher percent production being NG reveal that the other companies in the comparison have a higher earnings multiple than ARD. In other words 2 other companies that are fundamentally inferior with slower growth prospects have an unjustified earnings multiple premium when compared to ARD.

For example UPL is growing production, revenues, net income and EPS slower than ARD (ARD has the better future prospects.) UPL also has a higher percent of production in NG. Currently the market is giving UPL an earnings multiple of 29 in comparison to the ARD earnings multiple of 28.

One other example of the ARD earnings multiple being lower than another company that produces a significantly lesser amount of oil as a percentage of total production is GMXR. GMXR has less than 10% production in oil. Also GMXR growth in production, revenues, net income and EPS is much slower than ARD. (ARD has the better future prospects.) Currently the market is giving GMXR an earnings multiple of 38 in comparison to the ARD earnings multiple of 28.

Since ARD will grow earnings faster than both UPL and GMXR we can also conclude that ARD currently has a lower foward PE than both UPL and GMXR.

Expect that ARD earnings multiple to continue to expand back into the mid 30's or higher.

What can we expect for Q3'06 earnings?

Revenues: $17.9 million........ (up from $14.69 mm in Q2'06)

Net Profit Margin: 42%......... (down from 43.8% in Q2'06.)

Net Income: $7.51 million.....(up from $6.44 mm in Q2'06.)

Share Count*: 15 million.......(up from 14.64mm in Q2'06.)

*(Fully diluted)

EPS: $0.50.......(Up from $0.44 in Q2'06/ $0.27 in Q3'05.)

The projected quarter over quarter decline in net profit margin is a result of the potential for "other expenses" increasing due to NYSE listing fee requirements of at most $150,000. We'll have to wait and see how much of the listing fees are expensed in the third quarter. In terms of EPS this ($150,000) amounts to one penny ($0.01.)

Ttm Earnings will increase to $1.40. Put a earnings multiple of 29 on these earnings and you have a share price of $40.60. A more realistic multiple would be 35. This would yield a share price of $49. (One Wall Street firm recently put a target price on ARD shares of $49.)

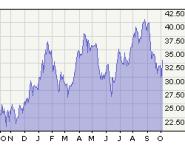

The 1 year chart below indicates that ARD has been making higher lows and higher highs.

ARD 1 Year Price Chart

Expect the trend to continue as ARD earnings per share increase over time. The three most important drivers of share price appreciation are earnings, earnings, earnings.

posted by -Aztec- at 2:37 PM

![]()

<< Home