ARD v GMXR Part III

Cost Structure and Production are Key

The purpose of today's post is to make sure everyone has a good understanding of why GMXR will have limited upside potential from the current share price of $36. This information is provided to give you the edge over those retail and institutional investors who may be looking to take advantage of the current valuation imbalance between ARD and GMXR. I want everyone to know that my intentions are to bring out analysis and commentary that has until now not been present. I think most of you would agree that the research provided by firms such as Hibernia don't present the in depth comparisons between ARD and GMXR and they don't address the problems associated with GMXR.

GMXR High Cost Structure

The main problem with owning GMXR at this time is the cost structure. When measuring total cost per BOE produced it is prohibitively high. This is especially true given the fact that GMXR is a gas company. Gas companies are supposed to have cost structures lower than their oil producing counterparts.

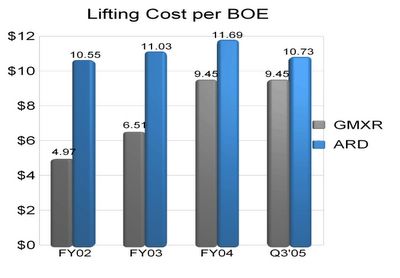

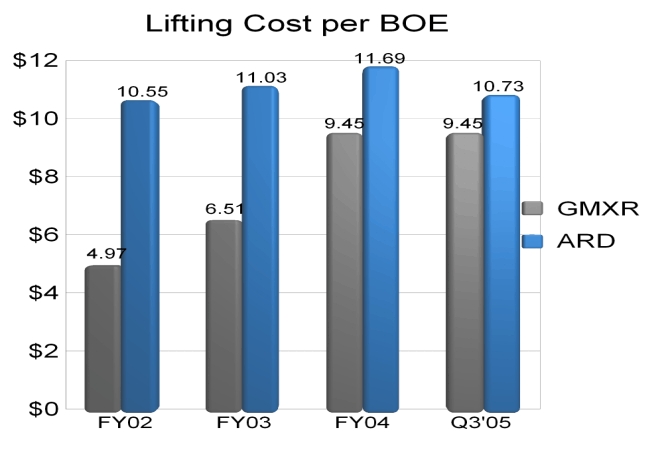

The counterpart I am specifically referring to is Arena Resources (ARD.) ARD has lifting costs that are slightly higher than GMXR. This is to be expected as ARD produces about 93% oil and 7% gas.

(Click on image to enlarge)

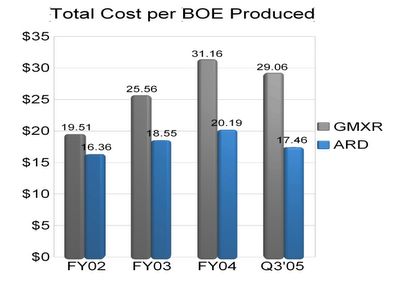

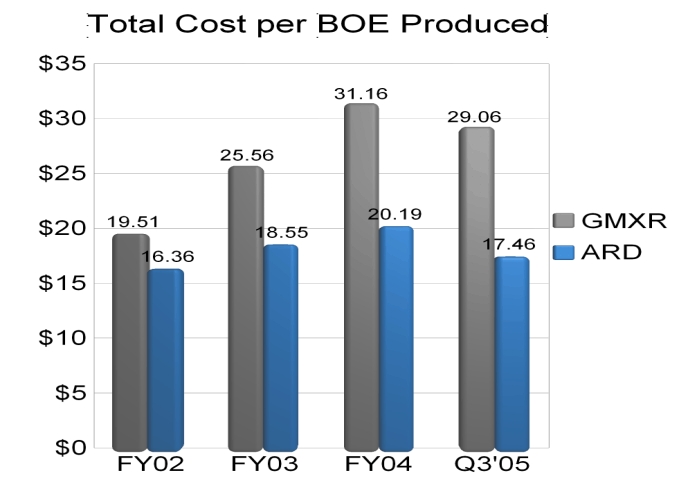

However, on a total cost per BOE produced basis ARD has a cost structure that has always been lower than that of GMXR. In fact, in the latest period measured ARD has total costs per BOE that are 66% below that of GMXR as noted in chart below.

(Click on image to enlarge)

ARD total cost structure is impossibly low. One should also examine the gap between GMXR total cost per BOE produced and that of ARD. Here is the total cost per BOE produced advantage that ARD has over GMXR:

FY2002.......$3.15 or 19%

FY2003.......$7.01 or 37%

FY2004.......$10.97 or 54%

Q3'05...........$11.60 or 66%

The gap has been widening in favor of ARD. I have every reason to believe that the ARD low cost advantage will continue to widen the gap and the trends that have been in place since 2002 will continue into 2006.

Unfortunately, the high cost structure at GMXR will keep a lid on not only earnings but also share price Share price appreciation potential will also be limited due to the current valuation imbalance with ARD. In other words the GMXR shares are overpriced.

Cost Structure Impacts Earnings

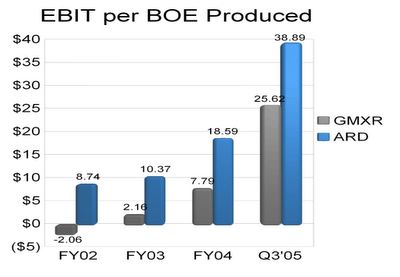

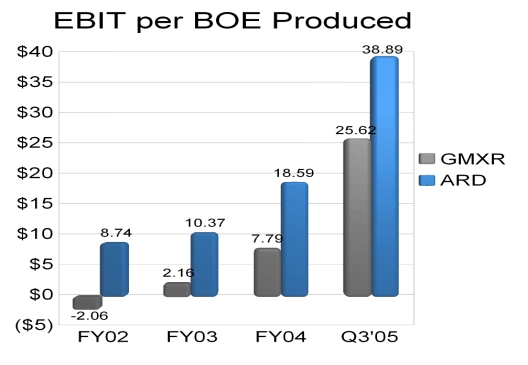

Due to the high GMXR cost structure it should be evident that GMXR will have the lower Earnings Before Income Tax (EBIT) per BOE produced and ARD will have the higher EBIT per BOE produced (and ultimately the higher profit margin.) The chart below shows this comparison.

(click on image to enlarge)

Production in 2006

If you examine the Hibernia research report for ARD dated 9-26-05 you will note that ARD is scheduled to produce over 1.1 million BOE for FY2006. (See Production Summary on Page 12.)

One day after GMXR announced the acquisition of another drilling rig Hibernia came out with a updated research report on GMXR. In that report it was estimated that GMXR would produce just under 1.1 million BOE as a result of the additional rig.

People need to realize that since Hibernia made the call for ARD to produce over 1.1 million BOE for FY2006 ARD has since acquired a drilling rig. This event occurred on December 8, 2005. The drilling rig that was acquired by ARD in December will when up and running effectively DOUBLE their drilling capability.

This rig is scheduled to be up and drilling by the start of Q2. Therefore, it should be easy for ARD to INCREASE PREVIOUSLY ESTIMATED 2006 production of 1.1 million BOE by MORE than 50% based on this fact. However lets be conservative and assume 0% (ZERO) growth.

In any case ARD is scheduled to produce more BOE in FY2006 than GMXR even without the ARD acquisition of a second drilling rig.

Cost Structure and Production

There are two very big reasons why ARD will not only earn more per share in 2006 and consequently have the higher share price. The reasons are as follows:

1. ARD has the SIGNIFICANTLY LOWER cost structure (66% lower.) As a consequence, ARD will continue to earn more for every BOE produced than GMXR in 2006.

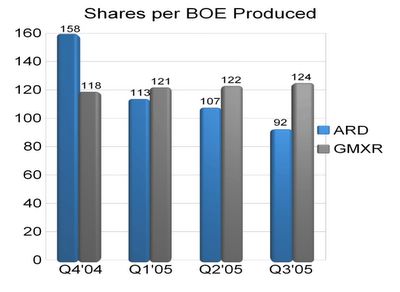

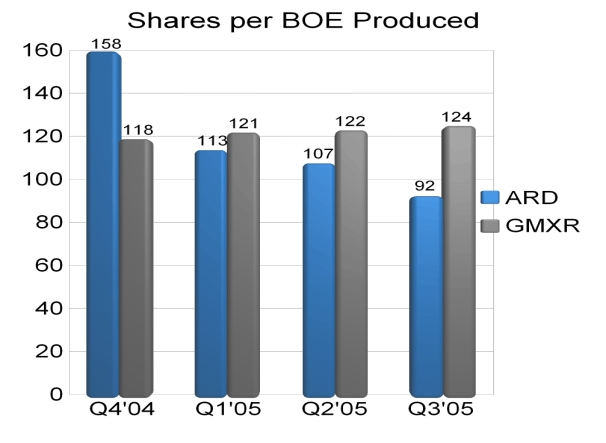

2. ARD has more production capability and will outproduce GMXR in 2006. ARD will also continue to exceed GMXR in terms of production per share as noted in my shares per BOE produced analysis.

(click on image to enlarge)

Cost Structure and Production are Key

The purpose of today's post is to make sure everyone has a good understanding of why GMXR will have limited upside potential from the current share price of $36. This information is provided to give you the edge over those retail and institutional investors who may be looking to take advantage of the current valuation imbalance between ARD and GMXR. I want everyone to know that my intentions are to bring out analysis and commentary that has until now not been present. I think most of you would agree that the research provided by firms such as Hibernia don't present the in depth comparisons between ARD and GMXR and they don't address the problems associated with GMXR.

GMXR High Cost Structure

The main problem with owning GMXR at this time is the cost structure. When measuring total cost per BOE produced it is prohibitively high. This is especially true given the fact that GMXR is a gas company. Gas companies are supposed to have cost structures lower than their oil producing counterparts.

The counterpart I am specifically referring to is Arena Resources (ARD.) ARD has lifting costs that are slightly higher than GMXR. This is to be expected as ARD produces about 93% oil and 7% gas.

(Click on image to enlarge)

However, on a total cost per BOE produced basis ARD has a cost structure that has always been lower than that of GMXR. In fact, in the latest period measured ARD has total costs per BOE that are 66% below that of GMXR as noted in chart below.

(Click on image to enlarge)

ARD total cost structure is impossibly low. One should also examine the gap between GMXR total cost per BOE produced and that of ARD. Here is the total cost per BOE produced advantage that ARD has over GMXR:

FY2002.......$3.15 or 19%

FY2003.......$7.01 or 37%

FY2004.......$10.97 or 54%

Q3'05...........$11.60 or 66%

The gap has been widening in favor of ARD. I have every reason to believe that the ARD low cost advantage will continue to widen the gap and the trends that have been in place since 2002 will continue into 2006.

Unfortunately, the high cost structure at GMXR will keep a lid on not only earnings but also share price Share price appreciation potential will also be limited due to the current valuation imbalance with ARD. In other words the GMXR shares are overpriced.

Cost Structure Impacts Earnings

Due to the high GMXR cost structure it should be evident that GMXR will have the lower Earnings Before Income Tax (EBIT) per BOE produced and ARD will have the higher EBIT per BOE produced (and ultimately the higher profit margin.) The chart below shows this comparison.

(click on image to enlarge)

Production in 2006

If you examine the Hibernia research report for ARD dated 9-26-05 you will note that ARD is scheduled to produce over 1.1 million BOE for FY2006. (See Production Summary on Page 12.)

One day after GMXR announced the acquisition of another drilling rig Hibernia came out with a updated research report on GMXR. In that report it was estimated that GMXR would produce just under 1.1 million BOE as a result of the additional rig.

People need to realize that since Hibernia made the call for ARD to produce over 1.1 million BOE for FY2006 ARD has since acquired a drilling rig. This event occurred on December 8, 2005. The drilling rig that was acquired by ARD in December will when up and running effectively DOUBLE their drilling capability.

This rig is scheduled to be up and drilling by the start of Q2. Therefore, it should be easy for ARD to INCREASE PREVIOUSLY ESTIMATED 2006 production of 1.1 million BOE by MORE than 50% based on this fact. However lets be conservative and assume 0% (ZERO) growth.

In any case ARD is scheduled to produce more BOE in FY2006 than GMXR even without the ARD acquisition of a second drilling rig.

Cost Structure and Production

There are two very big reasons why ARD will not only earn more per share in 2006 and consequently have the higher share price. The reasons are as follows:

1. ARD has the SIGNIFICANTLY LOWER cost structure (66% lower.) As a consequence, ARD will continue to earn more for every BOE produced than GMXR in 2006.

2. ARD has more production capability and will outproduce GMXR in 2006. ARD will also continue to exceed GMXR in terms of production per share as noted in my shares per BOE produced analysis.

(click on image to enlarge)

Shares per BOE indicates the number of shares required in order to "own" one BOE of production. Note how ARD shares per BOE produced has been dropping for each and every quarter while GMXR shares per BOE produced has been rising for each and every quarter. Put another way, production per share is increasing at ARD and decreasing at GMXR.

In conclusion, with the combination of ARD being able to earn more for every BOE produced AND and the ability to produce more BOE both in absolute terms and on a per share basis it should be elementary that ARD EPS will exceed that of GMXR in 2006. On this basis alone ARD shares would offer the more compelling investment. However, in previous posts it has been determined that ARD is the superior franchise to GMXR in virtually every statistic. ARD valuation is poised to surpass that of GMXR not only in terms of the various ratios that include Price to Earnings and Price to Sales but also in terms of share price.

posted by -Aztec- at 12:57 PM

![]()

<< Home