The Affects of NYMEX Crude Oil at $75 on ARD Valuation

In the March 10th post ARD valuation was discussed. At that time crude oil was much lower than today. In fact in that post we modeled ARD valuation based on an average realized price of $58. However with NYMEX crude oil now trading at over $75 a barrel we need to go back and take another look at valuation.

With NYMEX above $75 a barrel on crude oil that means the West Texas Intermediate prices will be about $71 or discounted about $4. Since we are not even in the summer driving and hurricane season we can expect oil prices to be much higher than they are today. To keep things simple lets assume that $71 will be our average realized price for FY2006 (This is being extremely conservative.) Lets also factor in NG sales that comprise about 17% of total production. Lets assume NG sells for $7 per Mcf. This means that each BOE of NG will sell for $42. (Keep in mind that the SEC states that there are 6 Mcfe per BOE of Natural Gas.)

The math is as follows:

$7 X 6 = $42.

ARD should produce about 1,000,000 BOE in 2006. Based on historical trends of 83% crude oil and 17% natural gas FY 2006 production would be as follows:

*830,000 BOE Crude Oil.......(83%)

*170,000 BOE Natural Gas...(17%)

Crude Revenues will be as follows:

830,000 X $71 =$58.93 million

Natural Gas Revenues will be as follows:

170,000 X $42*= $7.14 million

*(Remember 6 Mcfe at $7 per Mcf = $42 per BOE of NG)

Total Oil and Gas Revenues will be $66.07 million.

The equates to $66.07 per BOE produced.

(Click on image to enlarge)

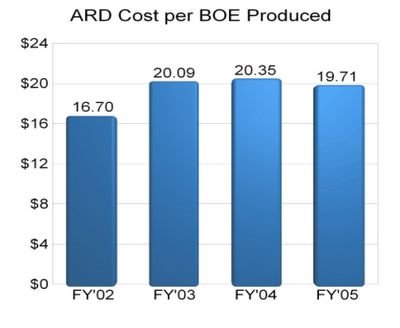

Our Costs per BOE should be less than $20 per BOE produced. Therefore ARD should have EBIT* per BOE produced of about $46 in FY2006 ($66 - $20 = $46)

*(EBIT = Earnings Before Income Tax)

Assuming 1,000,000 BOE produced this generates EBIT of $46 million.

Lets assume a tax rate of 25%.

$46 million X .25 = $11.5 million.

Lets subtract out the taxes to arrive at our final net profit:

$46 million (EBIT)- $11.5 million (Taxes) = $34.5 million Net Profits

Lets assume 14.8 million shares outstanding.

$34.5 million (Net Profits) / 14.8 million (Shares) = $2.33 EPS.

Put a conservative PE of 25 on the EPS to arrive at a target price of:

$2.33 (EPS) X 25 (PE) = $58.25 Share Price

While this is no big jump above our March 10th estimate it does take into account the increased natural gas production as a percentage of total production as well as factoring in a larger share count to be ultra conservative.

Keep in mind that ARD has a better chance of having a higher PE than 25.

The affects of the following PE multiples:

PE = 30

30X $2.33 = $69.90

At $69.90 we are trading at 51% of our target price with 93% price appreciation potential.

PE = 35

35X $2.33 = $81.55

At $81.55 we are trading at 44% of our target price with 125% price appreciation potential.

If investors invest in oil like the internet of the late 1990's we could get a PE on ARD that blows past 35X. Considering that an inferior company like GMXR carries a PE north of 50X earnings, it isn't out of the question for ARD to have a rising PE multiple as oil prices rise into the $80s and $90s this summer.

In the March 10th post ARD valuation was discussed. At that time crude oil was much lower than today. In fact in that post we modeled ARD valuation based on an average realized price of $58. However with NYMEX crude oil now trading at over $75 a barrel we need to go back and take another look at valuation.

With NYMEX above $75 a barrel on crude oil that means the West Texas Intermediate prices will be about $71 or discounted about $4. Since we are not even in the summer driving and hurricane season we can expect oil prices to be much higher than they are today. To keep things simple lets assume that $71 will be our average realized price for FY2006 (This is being extremely conservative.) Lets also factor in NG sales that comprise about 17% of total production. Lets assume NG sells for $7 per Mcf. This means that each BOE of NG will sell for $42. (Keep in mind that the SEC states that there are 6 Mcfe per BOE of Natural Gas.)

The math is as follows:

$7 X 6 = $42.

ARD should produce about 1,000,000 BOE in 2006. Based on historical trends of 83% crude oil and 17% natural gas FY 2006 production would be as follows:

*830,000 BOE Crude Oil.......(83%)

*170,000 BOE Natural Gas...(17%)

Crude Revenues will be as follows:

830,000 X $71 =$58.93 million

Natural Gas Revenues will be as follows:

170,000 X $42*= $7.14 million

*(Remember 6 Mcfe at $7 per Mcf = $42 per BOE of NG)

Total Oil and Gas Revenues will be $66.07 million.

The equates to $66.07 per BOE produced.

(Click on image to enlarge)

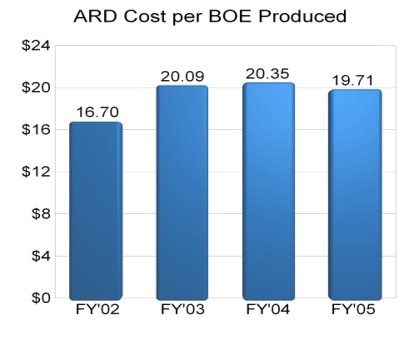

Our Costs per BOE should be less than $20 per BOE produced. Therefore ARD should have EBIT* per BOE produced of about $46 in FY2006 ($66 - $20 = $46)

*(EBIT = Earnings Before Income Tax)

Assuming 1,000,000 BOE produced this generates EBIT of $46 million.

Lets assume a tax rate of 25%.

$46 million X .25 = $11.5 million.

Lets subtract out the taxes to arrive at our final net profit:

$46 million (EBIT)- $11.5 million (Taxes) = $34.5 million Net Profits

Lets assume 14.8 million shares outstanding.

$34.5 million (Net Profits) / 14.8 million (Shares) = $2.33 EPS.

Put a conservative PE of 25 on the EPS to arrive at a target price of:

$2.33 (EPS) X 25 (PE) = $58.25 Share Price

While this is no big jump above our March 10th estimate it does take into account the increased natural gas production as a percentage of total production as well as factoring in a larger share count to be ultra conservative.

Keep in mind that ARD has a better chance of having a higher PE than 25.

The affects of the following PE multiples:

PE = 30

30X $2.33 = $69.90

At $69.90 we are trading at 51% of our target price with 93% price appreciation potential.

PE = 35

35X $2.33 = $81.55

At $81.55 we are trading at 44% of our target price with 125% price appreciation potential.

If investors invest in oil like the internet of the late 1990's we could get a PE on ARD that blows past 35X. Considering that an inferior company like GMXR carries a PE north of 50X earnings, it isn't out of the question for ARD to have a rising PE multiple as oil prices rise into the $80s and $90s this summer.

posted by -Aztec- at 12:25 PM

![]()

<< Home