How to Determine GMXR & ARD Valuation

ARD is a an Easy Double in 2006 while GMXR is Headed Lower

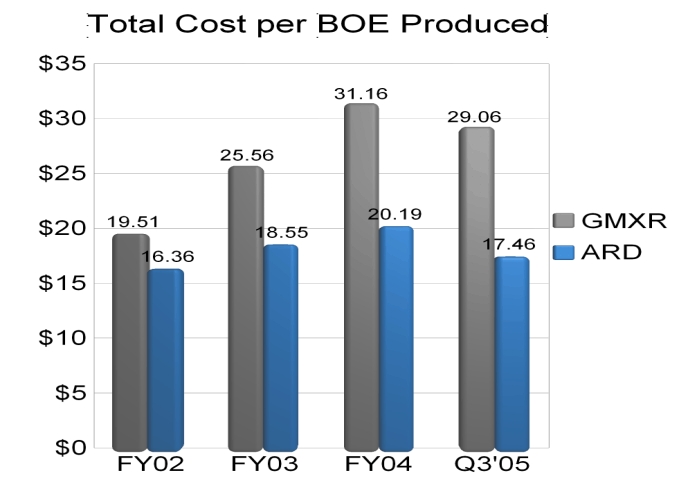

My Open Letter to GMXR Shareholders (See Open Letter here) details in the latest comparable period (Q3'05) the margin between revenue of each "GMXR BOE" generated and total cost per BOE produced. Keep in mind that a "GMXR BOE" is comprised of 6 mcfe (SEC says 6mcf = 1 BOE.)

I also examined the margin between the value of an "ARD BOE" and ARD total cost per BOE produced. Note that SEC says 1 BBL Oil = 1 BOE. The Value of each BOE is as follows:

GMXR: $39*

ARD: $58**

*based on $6.50 per Mcf

**based on $60 per Bbl of CL

(Click here to see total cost per BOE produced for both GMXR and ARD.)

The resultant margin between VALUE of each BOE and TOTAL COST OF EACH BOE PRODUCED is as follows:

GMXR: $9.94

ARD: $40.54

ARD is scheduled to produce a higher amount of BOE than GMXR in 2006.

GMXR Estimates are as follows:

First Albany Capital: 1,068,333 BOE

Ferris, Baker Watts, Inc.: 997,238 BOE

ARD Estimates are as follows:

Hibernia: 1,102,440 BOE

C.K. Cooper: 1,156,000 BOE*

M.S.Howells: 1,240,000 BOE*

DE Research: 1,089,000 BOE*

*(Note: Not posted on ARD website but available via Investor Relations)

The average GMXR 2006 production estimate:

1,032,785 BOE

The average ARD 2006 production estimate:

1,146,860 BOE

ARD is projected to produce 11% more BOE in 2006 than GMXR!

However to keep the math simple lets assume that both companies produce 1,000,000 BOE. 2006 EBIT will be as follows:

GMXR: $9.94 million.

ARD: $40.54 million.

Lets assume that each company pays 25% in taxes.

The 2006 net income would be as follows:

GMXR: $7.45 million

ARD: $30.40 million

Assume shares outstanding as follows:

GMXR: 11.1 million shares

ARD: 13.1 million shares

2006 EPS would be as follows:

GMXR: $0.67

ARD: $2.32

ARD has the more compelling earnings growth potential. Therefore it deserves a higher multiple. However to illustrate why ARD is the company that is GROSSLY UNDERVALUED with the EXTREMELY COMPELLING INVESTMENT POTENTIAL and why GMXR is GROSSLY OVERVALUED with ZERO COMPELLING INVESTMENT POTENTIAL lets give each company an identical PE multiple of 25.

EPS X PE = Share price.

GMXR: $0.67 X 25 = $16.75

ARD: $2.32 X 25 = $58

Since ARD has the higher growth in production, higher margin for each BOE produced, lower cost structure, stronger balance sheet and better fundamentals ARD deserves a higher PE multiple than GMXR. (Not to mention that ARD mgmt already has experience in selling a public company to a larger company. They sold NYSE Listed Magnum Hunter Resources to Cimarex.) Also keep in mind that ARD is scheduled to produce 11% more BOE in 2006 than GMXR therefore the estimated fair street value of $58 is extremely conservative. The very fact that ARD shares are priced at $27 and have a fair street value of at least $58 based on current CL prices is why I am table pounding this stock as a VERY STRONG BUY. ARD is an easy double in 2006.

On the otherhand I"m also table pounding GMXR as a VERY STRONG SELL based on the fact that it is currently priced at $30 with a fair street value of $17. I'll continue to blog about this gross imbalance in value between ARD and GMXR. I would recommend GMXR shareholders to profit from irrational market by selling the GMXR shares and purchasing ARD shares. It would be very prudent to trade in your overvalued GMXR shares while they still have a higher "currency" value over the undervalued ARD shares.

Note: Many GMXR shareholders have agendas. (They don't want you to sell your shares before they do!) I have no agenda other than to educate and raise the red flags on GMXR overvaluation! I am neither long nor short GMXR.

ARD is a an Easy Double in 2006 while GMXR is Headed Lower

My Open Letter to GMXR Shareholders (See Open Letter here) details in the latest comparable period (Q3'05) the margin between revenue of each "GMXR BOE" generated and total cost per BOE produced. Keep in mind that a "GMXR BOE" is comprised of 6 mcfe (SEC says 6mcf = 1 BOE.)

I also examined the margin between the value of an "ARD BOE" and ARD total cost per BOE produced. Note that SEC says 1 BBL Oil = 1 BOE. The Value of each BOE is as follows:

GMXR: $39*

ARD: $58**

*based on $6.50 per Mcf

**based on $60 per Bbl of CL

(Click here to see total cost per BOE produced for both GMXR and ARD.)

The resultant margin between VALUE of each BOE and TOTAL COST OF EACH BOE PRODUCED is as follows:

GMXR: $9.94

ARD: $40.54

ARD is scheduled to produce a higher amount of BOE than GMXR in 2006.

GMXR Estimates are as follows:

First Albany Capital: 1,068,333 BOE

Ferris, Baker Watts, Inc.: 997,238 BOE

ARD Estimates are as follows:

Hibernia: 1,102,440 BOE

C.K. Cooper: 1,156,000 BOE*

M.S.Howells: 1,240,000 BOE*

DE Research: 1,089,000 BOE*

*(Note: Not posted on ARD website but available via Investor Relations)

The average GMXR 2006 production estimate:

1,032,785 BOE

The average ARD 2006 production estimate:

1,146,860 BOE

ARD is projected to produce 11% more BOE in 2006 than GMXR!

However to keep the math simple lets assume that both companies produce 1,000,000 BOE. 2006 EBIT will be as follows:

GMXR: $9.94 million.

ARD: $40.54 million.

Lets assume that each company pays 25% in taxes.

The 2006 net income would be as follows:

GMXR: $7.45 million

ARD: $30.40 million

Assume shares outstanding as follows:

GMXR: 11.1 million shares

ARD: 13.1 million shares

2006 EPS would be as follows:

GMXR: $0.67

ARD: $2.32

ARD has the more compelling earnings growth potential. Therefore it deserves a higher multiple. However to illustrate why ARD is the company that is GROSSLY UNDERVALUED with the EXTREMELY COMPELLING INVESTMENT POTENTIAL and why GMXR is GROSSLY OVERVALUED with ZERO COMPELLING INVESTMENT POTENTIAL lets give each company an identical PE multiple of 25.

EPS X PE = Share price.

GMXR: $0.67 X 25 = $16.75

ARD: $2.32 X 25 = $58

Since ARD has the higher growth in production, higher margin for each BOE produced, lower cost structure, stronger balance sheet and better fundamentals ARD deserves a higher PE multiple than GMXR. (Not to mention that ARD mgmt already has experience in selling a public company to a larger company. They sold NYSE Listed Magnum Hunter Resources to Cimarex.) Also keep in mind that ARD is scheduled to produce 11% more BOE in 2006 than GMXR therefore the estimated fair street value of $58 is extremely conservative. The very fact that ARD shares are priced at $27 and have a fair street value of at least $58 based on current CL prices is why I am table pounding this stock as a VERY STRONG BUY. ARD is an easy double in 2006.

On the otherhand I"m also table pounding GMXR as a VERY STRONG SELL based on the fact that it is currently priced at $30 with a fair street value of $17. I'll continue to blog about this gross imbalance in value between ARD and GMXR. I would recommend GMXR shareholders to profit from irrational market by selling the GMXR shares and purchasing ARD shares. It would be very prudent to trade in your overvalued GMXR shares while they still have a higher "currency" value over the undervalued ARD shares.

Note: Many GMXR shareholders have agendas. (They don't want you to sell your shares before they do!) I have no agenda other than to educate and raise the red flags on GMXR overvaluation! I am neither long nor short GMXR.

posted by -Aztec- at 10:33 PM

![]()

{kind=link}

<< Home