Analysis of Anadarko's Acquisition of WGR Indicates ARD Significantly Undervalued

Valuing WGR E&P Segment

On June 23, 2006 Anadarko acquired Western Gas Resources (WGR) for $61 per share in cash. The press release issued by WGR stated, "The per share consideration payable in the merger represents a premium of approximately 49 percent over Western's closing stock price on June 22, 2006. The transaction is valued at approximately $5.3 billion, including approximately $560 million in indebtedness." By digesting this acquisition we are not only able to measure the value of the various business segments of WGR but to also confirm the intrinsic value of ARD shares.

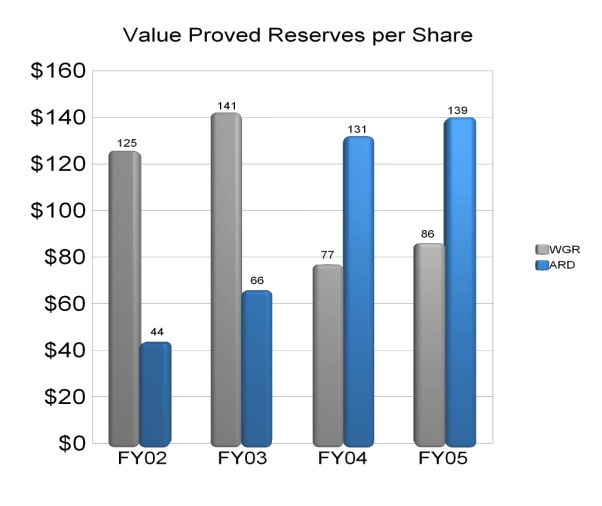

Let us begin by first looking at the value of proved reserves per share. Our calculations are based on $65 oil and $7 gas. The results below are depicted in figure 1.

Figure 1. (Click on Image to Enlarge)

It should be noted that ARD Value Proved Reserves per Share (VPRPS) has increased in every year since 2002. WGR had a 2 for 1 stock split in 2004 thereby reducing its VPRPS by 50%. In any case, ARD has significantly more VPRPS than WGR in 2005:

ARD....$139

WGR.....$86

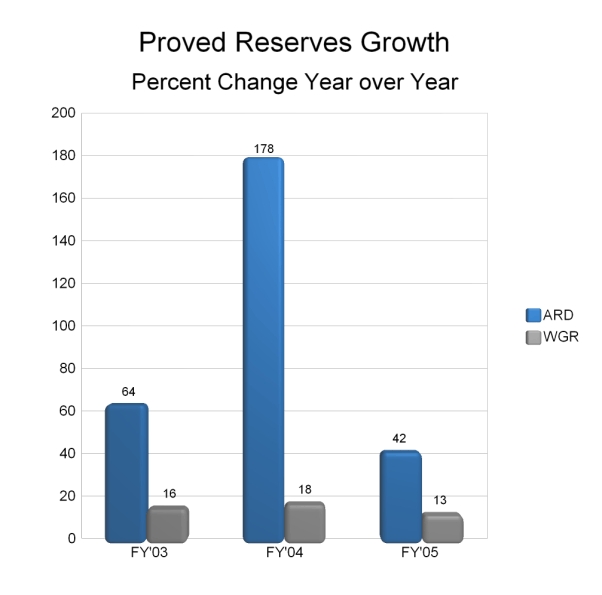

Now lets take a look at the historical trends in proved reserves growth. Figure 2 below illustrates the percent growth year over year in proved reserves.

Figure 2. (Click on Image to Enlarge)

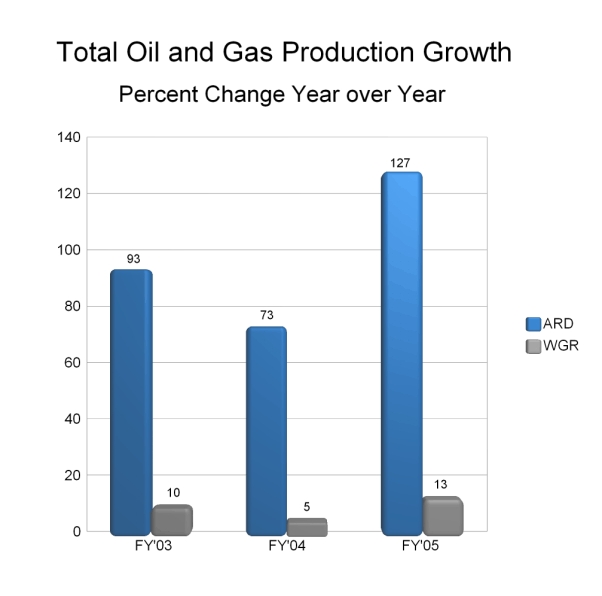

It should be noted that ARD has been growing proved reserves significantly faster than WGR since 2002. Figure 3 below indicates that ARD also has superior production growth when compared to WGR.

Figure 3. (Click on Image to Enlarge)

It really is amazing how ARD production has been more than doubling every year for the last three years. The same can not be said about WGR production.

It should also be noted that ARD has 82% oil proved reserves to less than 3% for that of WGR. Given the fact that:

1. Oil spare capacity is razor thin and

2. Natural gas does not exhibit the same tight supplies as oil and

3. 70% of oil is used for transportation purposes in the production of gasoline in which there is no substitute and

4. Natural gas can be substituted with coal and nuclear power and

5. The world's thirst for oil is increasing at a time when maintaining current levels of production let alone increasing it is becoming more difficult with every passing day

Be it resolved that future oil prices are going higher while natural gas is headed flat to lower. Gas has less intrinsic value than oil. Therefore, the intrinsic value of companies with a higher percentage natural gas are less than those companies that have a higher percentage of proved reserves oil all other things being equal.

The target price on ARD is $60. This represents 43% of VPRPS.

$60 (Target Price)/$139 (VPRPS*) = 43%

*VPRPS = Value Proved Reserves per Share; See Figure 1.

If we also take 43% of WGR VPRPS of $86 we come up with a target price of $36.98 (rounded to $37) based on the company's E&P segment. Since ARD is not only growing proved reserves and production faster than WGR but also has a higher percentage of oil we must discount the intrinsic value or target price of WGR based on VPRPS. Since we valued ARD at 43% of VPRPS we should value WGR at something less than this amount. A 10% discount would be very conservative and favorable to WGR shareholders.

Fair value of ARD is 43% of VPRPS.

WGR E&P operations should be valued at a 10% discount to ARD's fair value ratio of 43% of VPRPS. Therefore, WGR fair value ratio is 38.7% of VPRPS. The math is as follows:

43% X .10 = 4.3%

43% - 4.3% = 38.7%

WGR VPRPS is $86. If we multiply this amount by 38.7% we have arrived at a per share valuation of the E&P segment of WGR. This amount comes out to be $33.28.

$86 X .387 = $33.28

With 76.01 million shares outstanding the value of this segment is $2.529 billion.

Valuing WGR Natural Gas Gathering, Processing & Treating Facilities Segments

These segments of WGR are comparable to those of Holly Corp (HOC.) Holly Corp has a market cap of $2.75 billion. Lets make some comparisons between HOC and WGR in order to determine a valuation of these segments of the WGR business.

Revenue ttm:

WGR...$3.54 B

HOC....$3.38B

Profit Margin ttm:

WGR...3.9%

HOC....5.94%

Operating Margin ttm:

WGR...7.7%

HOC....8.32%

Net Income ttm:

WGR...$141 million

HOC....$183 million

Shares:

WGR...76.01 million

HOC....57.45 million

EPS:

WGR...$1.85

HOC....$3.18

Debt:

WGR...$560 million

HOC....No debt

Since the revenues are of the same magnitude lets assume for a moment that both companies deserve the same market cap. HOC has a market cap of $2.75 billion with no debt. WGR has debt of about $560 million. To keep our comparison of these two companies comparable we must reduce the value of the WGR assumed market cap of $2.75B by $560 million. If we subtract $2.75B by $560 million we arrive at $2.19 billion.

Since HOC has superior fundamentals to WGR it would be prudent to discount WGR. Let us discount these segments of the WGR business by an amount that is both conservative and favorable to WGR shareholders. This amount shall be 3.7% ($82 million to be exact.)

$2.19B - $82 million = $2.108 billion

With 76.01 million shares outstanding the value of these business segments per share is $27.73

Valuing All Segments of WGR

Previously we determined that the value of the E&P segment was worth $2.529B or $33.28 per share based on 76.01 million shares. We also determined that the natural gas gathering, processing and treating facilities segments were worth $2.108B or $27.73 per share based on 76.01 million shares. If we add these amounts we come up with $4.637 billion or $61.01 per share. There were also approximately 1.69 million shares of restricted stock and stock options that were automatically converted and paid out at $61 per share. This effectively raised the value of the transaction another $103 million from $4.637 billion to $4.74 billion. If we add the debt of $560 million to the sum of $4.74 billion we arrive at a total transaction purchase price of $5.3 billion.

What We Have Learned from Analyzing the Value of the Various WGR Segments

By using Holly Corp as a benchmark of valuation for the WGR natural gas gathering, processing and treating facilities segments and ARD as a benchmark of valuation for the WGR E&P segment we were able to get a better understanding of what Anadarko really paid in order to acquire WGR. Not only did Anadarko pay full price for the right to acquire WGR assets but they also paid a fair price.

In conclusion, analysis of the Anadarko acquisition of WGR has allowed us to not only measure the value of the various business segments of WGR but to also confirm the intrinsic value of ARD shares. This is done by a process of "Reverse benchmarking." In other words, after logically assigning a value to each business segment by breaking down the total value of the transaction we have determined that the superior fundamentals and proved reserves of ARD are indeed worth at least $60 per share. With oil rising to $75.19 and gas continuing to fall to $5.76 the Crude oil/ NG ratio has risen to 13.05X. As this ratio continues to expand, expect those fundamentally superior companies with the majority of their proved reserves in oil to become increasingly popular with investors. There is every reason to believe that 2006 will be an extremely rewarding year for ARD investors as the shares advance towards $60 before year end.

posted by -Aztec- at 11:16 PM

![]()

<< Home