GMXR Valuation Based on Business and Fundamentals

Legislation Introduced Could Force GMXR Shareholders to Re-Examine Valuation of Shares

There is legislation regarding oil and gas mergers that could gain momentum as congress and examines the issues of rising oil and gas prices. While it is a political hot potato to legislate windfall profits taxes (they don't work), restricting mergers and acquisitions in the name of increased competition and lower prices is something most legislators would think is reasonable. If a bill like this gains momentum this would force GMXR shareholders to take a hard look at the company's business operation of NG production as a GMXR buyout would no longer be a "slam dunk."

(Keep in mind that a GMXR buyout would no longer be a "slam dunk" if NG prices would drift below $6.50 per Mcfe...as margins would not be attractive for a potential suitor.)

EXAMINATION OF GMXR BUSINESS OPERATIONS

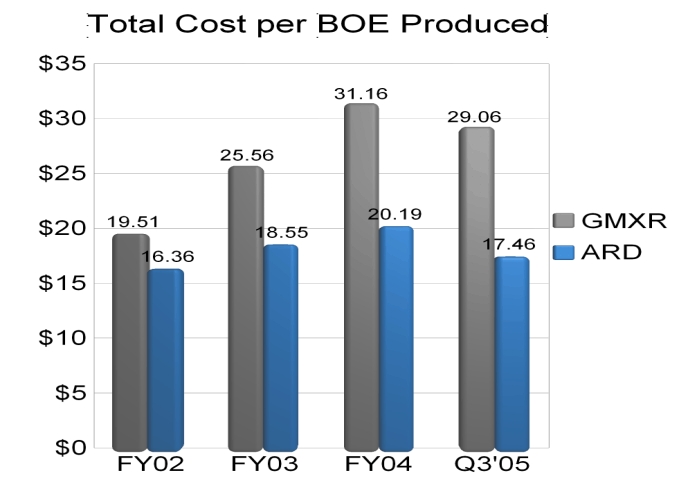

As I have pointed out it should be very clear that GMXR is a high cost producer of NG...not a low cost producer. With current prices there is very little margin of error between a profit and a loss for the quarter.

Case in Point:

With $6.50 NG the value of a GMXR BOE = $39

($6.50 X 6* = $39)

*SEC says 6mcfe = 1 BOE.

The difference between total cost per BOE and total revenue per BOE based on Q3'05 and $6.50 NG is:

Total Revenue per BOE: $39

Total Cost per BOE: $29.06*

Net Margin per BOE: $9.94

*Data taken from graph derived from various SEC filings.

(To illustrate how small the $9.94 GMXR net margin per BOE produced basis is it should be noted that ARD margin per BOE produced is about $40 or over 4X that of GMXR based based on $60 oil. It should also be noted that oil producers typically have a cost profile that is much higher than that of gas producers. With that said it should be crystal clear that GMXR cost structure is sky high while ARD cost structure is impossibly low.)

What is the affect of a 10% decline in NG prices?

Total revenue per BOE produced would drop from $39 to $35.10.

(Lets assume total cost per BOE produced would stay the same at $29.06.)

With a BOE of NG now valued at $35.10 now the margin would shrink from $9.94 to $6.04.

($35.10 - $29.06 = $6.04)

The reduction in Net Profit Margin per BOE as a result of the 10% decrease in NG prices would be $3.90

($9.94 - $6.04 = $3.90)

This ($3.90) represents a decrease of 39.2% in net margin per BOE produced.

($3.90 / $9.94 = .392)

My estimate for GMXR 2006 EPS is $0.67 based on $6.50 NG. With a 10% decline in NG prices from $6.50 to $5.85 there would be a decline of 39.2% in net profits.

($0.67 X .392 = $0.26)

That would reduce 2006 EPS from $0.67 to $0.41.

With a PE of 25 that would reduce the target price from $17 to $10.25

($0.41 X 25 = $10.25.)

My point of this discussion is to illustrate how close GMXR is to going off the edge of a cliff; The affects of the high cost structure on attracting a potential suitor; The realities of 2006 EPS analysts estimates being grossly overstated and the consequential CONTINUED future downward revisions of EPS.

Legislation Introduced Could Force GMXR Shareholders to Re-Examine Valuation of Shares

There is legislation regarding oil and gas mergers that could gain momentum as congress and examines the issues of rising oil and gas prices. While it is a political hot potato to legislate windfall profits taxes (they don't work), restricting mergers and acquisitions in the name of increased competition and lower prices is something most legislators would think is reasonable. If a bill like this gains momentum this would force GMXR shareholders to take a hard look at the company's business operation of NG production as a GMXR buyout would no longer be a "slam dunk."

(Keep in mind that a GMXR buyout would no longer be a "slam dunk" if NG prices would drift below $6.50 per Mcfe...as margins would not be attractive for a potential suitor.)

EXAMINATION OF GMXR BUSINESS OPERATIONS

As I have pointed out it should be very clear that GMXR is a high cost producer of NG...not a low cost producer. With current prices there is very little margin of error between a profit and a loss for the quarter.

Case in Point:

With $6.50 NG the value of a GMXR BOE = $39

($6.50 X 6* = $39)

*SEC says 6mcfe = 1 BOE.

The difference between total cost per BOE and total revenue per BOE based on Q3'05 and $6.50 NG is:

Total Revenue per BOE: $39

Total Cost per BOE: $29.06*

Net Margin per BOE: $9.94

*Data taken from graph derived from various SEC filings.

(To illustrate how small the $9.94 GMXR net margin per BOE produced basis is it should be noted that ARD margin per BOE produced is about $40 or over 4X that of GMXR based based on $60 oil. It should also be noted that oil producers typically have a cost profile that is much higher than that of gas producers. With that said it should be crystal clear that GMXR cost structure is sky high while ARD cost structure is impossibly low.)

What is the affect of a 10% decline in NG prices?

Total revenue per BOE produced would drop from $39 to $35.10.

(Lets assume total cost per BOE produced would stay the same at $29.06.)

With a BOE of NG now valued at $35.10 now the margin would shrink from $9.94 to $6.04.

($35.10 - $29.06 = $6.04)

The reduction in Net Profit Margin per BOE as a result of the 10% decrease in NG prices would be $3.90

($9.94 - $6.04 = $3.90)

This ($3.90) represents a decrease of 39.2% in net margin per BOE produced.

($3.90 / $9.94 = .392)

My estimate for GMXR 2006 EPS is $0.67 based on $6.50 NG. With a 10% decline in NG prices from $6.50 to $5.85 there would be a decline of 39.2% in net profits.

($0.67 X .392 = $0.26)

That would reduce 2006 EPS from $0.67 to $0.41.

With a PE of 25 that would reduce the target price from $17 to $10.25

($0.41 X 25 = $10.25.)

My point of this discussion is to illustrate how close GMXR is to going off the edge of a cliff; The affects of the high cost structure on attracting a potential suitor; The realities of 2006 EPS analysts estimates being grossly overstated and the consequential CONTINUED future downward revisions of EPS.

posted by -Aztec- at 11:57 AM

![]()

{kind=link}

<< Home