ARD Reserves Exceed Value of GMXR in Both Total and on a per Share Basis

Many people seem to think that GMXR proved reserves are more valuable than those of ARD. However if one takes a closer look it is evident that the ARD proved reserves are far more valuable than those of GMXR.

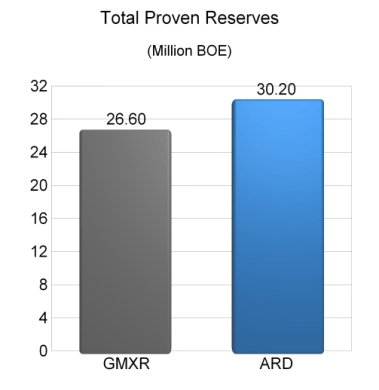

First lets take a look at the total proven reserves for both GMXR and ARD. The chart below shows the relationship in total proven reserves.

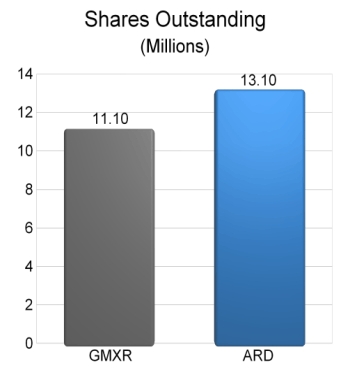

The chart above indicates that GMXR has slightly less proved reserves than ARD. However to have a better understanding of what the value of these reserves are to the share holder we need to determine the number of shares outstanding for both companies. The chart below shows the share count fully diluted for GMXR and ARD.

Our calculator indicates that GMXR has slightly more proved BOE per share than that of ARD.

The math looks like this:

GMXR:

26.6 mm BOE/11.1 mm shares=2.39 BOE per share.

ARD

30.2 mm BOE/13.1 mm shares=2.30 BOE per share.

At first glance it appears that the GMXR shares have more value than the ARD shares by virtue of the GMXR shares having more BOE per share. However it must be understood that the ARD and GMXR BOE each have a completely different value. Based on today's closing price for oil ($63.10) and the closing price for natural gas ($7.16) we can derive the following values per BOE for both GMXR and ARD:

GMXR: $42.96*

*(SEC says 1 BOE = 6 mcfe; $7.16 X 6 = $42.96)

ARD: $60**

**(Estimate based on fact that ARD also produces small amount of NG)

If we multiply the above BOE valuations by the number of BOE per share we can determine the Oil and Gas (O&G) assets per share valuation.

The math looks like this:

GMXR $42.96 X 2.39 = $102.67

ARD $ 60 X 2.3 = $138

With the above calculations it seems that ARD has a $35.33 advantage over GMXR in terms of O&G assets per share. In percentage terms ARD has over 34% more O&G assets per share.

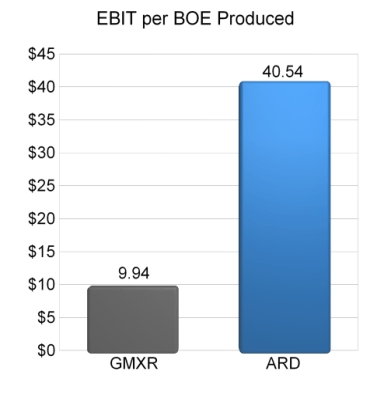

However we all know that in order to get a more reliable picture of the true intrinsic value of these reserves we must take into account the EBIT that each BOE produces. The chart below depicts the amount of EBIT per BOE produced in the latest comparable quarter (Q3'05).

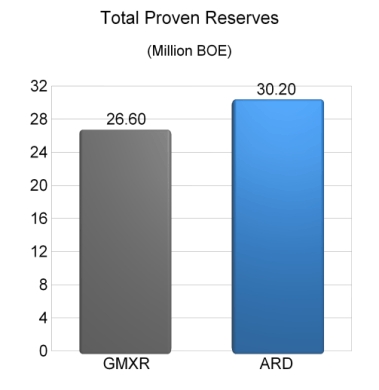

Now that we know the amount of EBIT per BOE produced lets again take a look at the chart that depicts the total proved BOE for each company.

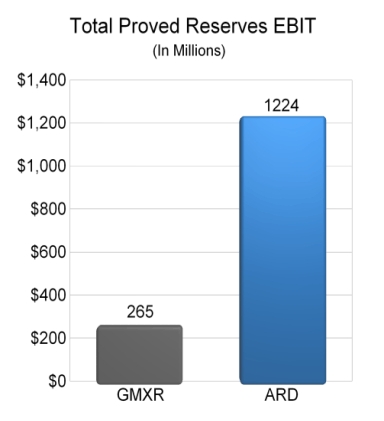

Based on the above proved reserve totals and the amount of EBIT per BOE produced we can determine the total amount of EBIT to be generated for each company.

The math is as follows:

GMXR:

26.6 mm BOE X $9.94 EBIT/BOE = $264.4 million.

(Lets round the $264.4 to $265 for easier math.)

ARD:

30.2 mm BOE X $40.54 EBIT/BOE = $1.224 BILLION.

With the above facts of GMXR proved reserves capable of generating EBIT of $265 million and ARD proved reserves capable of generating EBIT of $1.224 billion it is clear that ARD is capable of producing over 4.6 X more EBIT than GMXR. The chart below shows the comparison of total proved reserves EBIT.

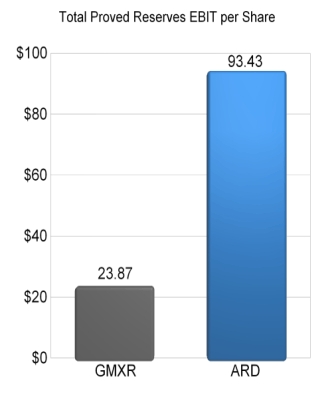

Now that we have the total EBIT that each proved reserve base is capable of producing we must now divide the amounts in the above chart by the total share count for each company to come up with the total EBIT per share.

The math looks like this:

GMXR: $265 million / 11.1 million = $23.87

ARD: $1.224 Billion/ 13.1 million = $93.43

The chart below compares the total proved reserves EBIT per share.

ARD is capable of generating over 3.9X more EBIT per share than GMXR ($93 to $23) even though GMXR has slightly more O&G assets per shares (2.39 to 2.3.) It should be crystal clear that the ARD reserves have much more value both in total and on a per share basis when compared to GMXR.

Based on GMXR current share price of $32.30 GMXR trades at over a 35% premium to the value of the EBIT per share based on the total proved reserves. Keep in mind that my 2006 target price on GMXR of $17 would put the share price below the proved reserve EBIT per share (40% discount to be exact) and would be a more realistic price and much closer to fair value.

In contrast, ARD current share price of $28.28 trades at a 230% discount to the EBIT per share based on total proved reserves. My 2006 price target on ARD of $60 would put ARD shares closer to a fair valuation and reduce the discount from 230% to a more reasonable 55% discount.

In summary it is easy to see that many investors are overestimating GMXR intrinsic value while at the same time grossly underestimating ARD intrinsic value. Valuing both GMXR and ARD reserves based on the amount of profit derived from each BOE and the actual number of BOE proved reserves per share it is easy to see that ARD shares have a much higher intrinsic value. This is a primary reason why ARD shares deserve to have a valuation that not only exceeds that of GMXR but exceeds that of GMXR by a wide margin. Even if GMXR proved reserves were doubled, ARD would still have more total proved reserves EBIT as well as proved reserves EBIT per share. Look for ARD share valuation to surpass that of GMXR in 2006 as the market begins to takes notice of these facts.

posted by -Aztec- at 12:26 PM

![]()

<< Home