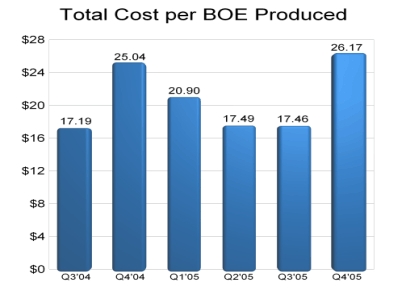

A Look Back to Q4 2004 Reveals that this has Happened Before. Everything is Normal.

While some people are worried that ARD had a bad quarter I say relax! Not all metrics improve in a linear fashion every single quarter. Every company has challenges and Q4 seems to be a quarter in which ARD has the most challenges. One need only go back to Q4 2004. Take a look at the chart below? Does the rise in total cost per BOE produced look familiar? The numbers are amazingly familiar! Notice how Q4 in 2004 also saw a similar rise in total cost per BOE produced. This is nothing new. Take it in stride. If Q1 2005 is any indication as to what Q1 2006 will be like I think we can look forward to the total cost per BOE produced to decline next quarter and net margins to rise from current levels.

(Click on Image to Enlarge.)

Lets break down what I projected and what ARD actually came in at (2005 10K.)

Average Realized Price:

Estimate...$55

Actual.....$54.30

(I was off by 1.2%)

Revenue:

Estimate...$9.48mm

Actual.....$9.36mm

(I overestimated by 1.2%)

Net Margin:

Estimate...44%

Actual.....32%

(I overestimated by 27%)

Net Income:

Estimate...$4.07mm

Actual.....$3.01mm

(I overestimated by 26%)

Share Count:

Estimate...12.99mm

Actual.....13.09mm

(I underestimated by less than 1%)

All in all I nailed the:

1. Average realized price

2. Revenue

3. Share count

I was surprised and way off on my net margin...as was everyone else I"m sure. I have some theories on why I believe net margin came in 12 points below what I estimated:

1. Drilling program creates a lot of expense. These expenses are rising faster than the flow of oil from the wellheads. Hopefully in the future once production is established the LOE will decrease as infrastructure is already in place and paid for. I"m thinking that with all the new wells there will be more infrastructure requirements than most investors realize. I think Tim and Stan will mention something to this effect.

2. Possible delays in getting wells producing oil and connected to the system after the well has been drilled. Edadjootian mentioned that one of his concerns was ARD poking all the holes in the ground they want but just not being able to get them connected and producing in a timely manner. This may have something to do with the Q4 production being less than I anticipated.

3. Production declines greater than 6% yearly are being experienced in the oil patch in my estimation. This is one reason why I revised my 2006 Year end estimate from from something north of 2 million BOE to exactly 1 million BOE. If you take into account the greater than normal production declines in concert with the infrastructure intensive drilling program you have a recipe for lowered margins. I failed to take that into account and underestimated costs and thereby overestimating net margins. I"m hopeful that in the future when the infrastructure is in place that the production costs will be much lower thereby allowing net margins to again rise.

Was Q4 a complete failure? Absolutely not!

If you compare the Q4 YoY numbers ARD IMPROVED! For example, look at the 10K on page 72.

*Net margin increased from 29% to 32%

*Fully diluted EPS increased over 144%

*Revenues increased more than 215%

*Production increased YoY by 167% and QoQ by 22%. That is EXCELLENT folks!

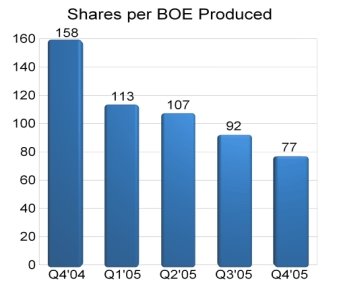

*Shares per BOE produced improved to 77.

(Shares per BOE produced is a metric that indicates how many shares of ARD you need to own in order to "own" 1 BOE of production.)

And even with our relative "disappointment" surrounding net margin...it was 32%. Not many companies can boast such a fat net margin. No doubt Q4 was a challenging quarter. However once we get the infrastructure in place, costs will decline and BOE produced will continue to rise. Historically Q4 has been a challenging quarter for the company. Last year Q4 production decreased QoQ. In Q3'04 production was 69,763. In Q4'04 production dropped to 64,494. So In light of the disappointment surrounding net margin in Q4'05 and higher than expected expenses I think it was a successful quarter. Keep in mind that Oil companies typically have a higher cost profile than NG companies...yet even in a challenging quarter such as this ARD was able to produce at a cost profile of $26.17 per BOE. This still beat GMXR with a cost profile of $28.69 per BOE produced.The future looks bright. A second rig will be coming online. With the increased wells and infrastructure already being put in place margins will increase as production continues to increase. Q4 was certainly not a step backwards. It was a step forward. Hopefully management will provide more transparency, guidance and updates so we have a better idea of what to expect and a better understanding of how our company functions.

posted by -Aztec- at 10:30 PM

![]()

<< Home