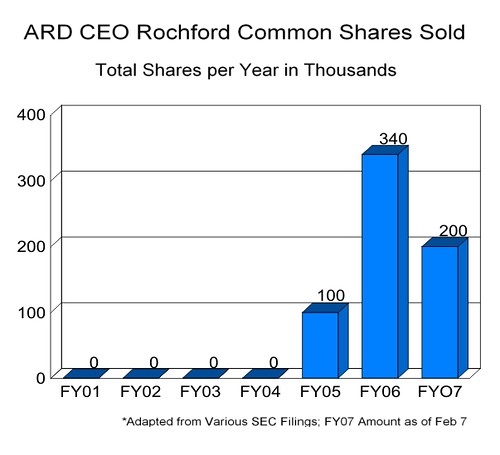

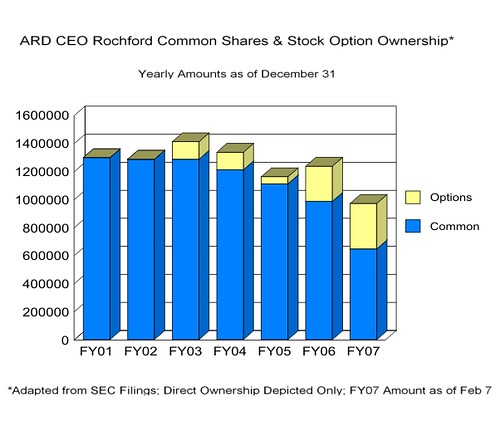

Why my ARD Share Count was Reduced 26% Today

Various Reasons Contributed to Decision; Diversification and More Attractive Investment Opportunity Played Key Role to Sell

Arena Resources' ratio of capex to cashflow from operating activities, EPS per dollar invested and the likely decline in future production growth were three primary factors that contributed to my decision to sell over a quarter of my ARD shares today. Such a sale never would have occurred in the absence of another more attractive investment opportunity.

The other company I moved the proceeds into was just far too undervalued based on the tremendous earnings power per dollar invested (topping that of ARD), cashflow from operating activities in excess of capex by a significant margin (unlike ARD) and production growth that is more secure without the great challenges of the natural declines that occur in mature oil fields such as the Fuhrman-Mascho.

The new company I invested in does not produce oil. It produces a commodity that has the same worldwide supply/demand issues that exist with that of oil. The peak oil problem will have the effect of increasing future demand for this non hydrocarbon as governments seek solutions to rising oil prices by investing in alternative fuels such as ethanol (stainless steel requirements) and hybrid vehicles (nicad batteries.) Both stainless steel and nicad batteries are only two of countless applications that consume a commodity the new company produces.

One should not construe my portfolio rebalancing as a result of glaring red flags at ARD. The more proper assessment would be that the other opportunity currently presents a more significant discount to intrinsic value than does ARD.

Going forward I do have certain expectations for ARD. Failure to meet or exceed my expectations would result in the possibility of future ARD liquidation. The expectations are as follows:

1. Oil in Kansas: The absence of commercial oil production associated with the deep test on the Syracuse in light of the Phil Terry promotion to COO at a salary of $160,000 a year would be a red flag. Only in the presence of oil in Kansas should Phil Terry have been hired. Lack of oil in Kansas noted in FY06 C.C. would yield a red flag.

2. EPS coming in at or Above $0.36: An EPS disappointment below my conservative estimate of $0.36 would yield another red flag. This would be a sign of a cost structure that is rising faster than expected.

3. Proved Reserve Growth of at Least 40.2%: Anything less than a 40.2% increase in year end proved reserves to 42,362,535 BOE for FY2006 would be considered a disappointment. This would constitute another possible red flag.

Even in the absence of potential red flags as mentioned above, a sound business decision could mandate the further decrease of ARD ownership and increase the ownership of the new company. The new company I have moved funds into as mentioned above is a producer of the base metal nickel. Here is the price history of the commodity. This company comprises the second company in my portfolio. After the release of ARD Q4'06 results this company will be revealed.

Various Reasons Contributed to Decision; Diversification and More Attractive Investment Opportunity Played Key Role to Sell

Arena Resources' ratio of capex to cashflow from operating activities, EPS per dollar invested and the likely decline in future production growth were three primary factors that contributed to my decision to sell over a quarter of my ARD shares today. Such a sale never would have occurred in the absence of another more attractive investment opportunity.

The other company I moved the proceeds into was just far too undervalued based on the tremendous earnings power per dollar invested (topping that of ARD), cashflow from operating activities in excess of capex by a significant margin (unlike ARD) and production growth that is more secure without the great challenges of the natural declines that occur in mature oil fields such as the Fuhrman-Mascho.

The new company I invested in does not produce oil. It produces a commodity that has the same worldwide supply/demand issues that exist with that of oil. The peak oil problem will have the effect of increasing future demand for this non hydrocarbon as governments seek solutions to rising oil prices by investing in alternative fuels such as ethanol (stainless steel requirements) and hybrid vehicles (nicad batteries.) Both stainless steel and nicad batteries are only two of countless applications that consume a commodity the new company produces.

One should not construe my portfolio rebalancing as a result of glaring red flags at ARD. The more proper assessment would be that the other opportunity currently presents a more significant discount to intrinsic value than does ARD.

Going forward I do have certain expectations for ARD. Failure to meet or exceed my expectations would result in the possibility of future ARD liquidation. The expectations are as follows:

1. Oil in Kansas: The absence of commercial oil production associated with the deep test on the Syracuse in light of the Phil Terry promotion to COO at a salary of $160,000 a year would be a red flag. Only in the presence of oil in Kansas should Phil Terry have been hired. Lack of oil in Kansas noted in FY06 C.C. would yield a red flag.

2. EPS coming in at or Above $0.36: An EPS disappointment below my conservative estimate of $0.36 would yield another red flag. This would be a sign of a cost structure that is rising faster than expected.

3. Proved Reserve Growth of at Least 40.2%: Anything less than a 40.2% increase in year end proved reserves to 42,362,535 BOE for FY2006 would be considered a disappointment. This would constitute another possible red flag.

Even in the absence of potential red flags as mentioned above, a sound business decision could mandate the further decrease of ARD ownership and increase the ownership of the new company. The new company I have moved funds into as mentioned above is a producer of the base metal nickel. Here is the price history of the commodity. This company comprises the second company in my portfolio. After the release of ARD Q4'06 results this company will be revealed.

posted by -Aztec- at 11:01 PM

![]()

{kind=link}