Why an Economic Slowdown in the USA Would Have Little Impact on World Oil Demand

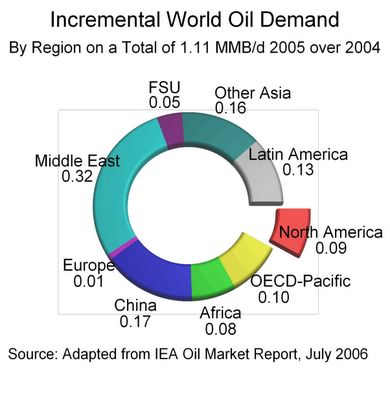

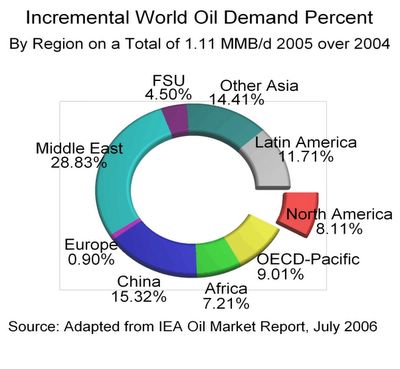

North American Incremental Oil Demand Accounted for only 8% of Total Between 2004 and 2005.

Between 2004 and 2005 world oil demand increased by 1.11 million barrels per day according to the International Energy Agency Oil Market Report dated July 2006. Of this incremental increase of 1.11 MMB/d demand in North America (USA and Canada) increased only 90,000 b/d as depicted in chart 1 below. In terms of percent this amount to just over 8% of the incremental world oil demand between 2004 and 2005 as depicted in chart 2 below.

Chart 1. (Click on Image to Enlarge)

Notice how the Middle East accounted for over 28% of the world incremental oil demand. This is nearly twice as much new demand as that of China between 2004 and 2005. With the new found oil wealth from rising oil prices the countries in the Middle East have vast amounts of money to spend on their economies. There is no doubt that the increase in GPD causes an increase in oil consumption. If you plot total Middle East GPD against total Middle East oil consumption you will see a line that increases against each axis. For more information on this phenomenon read chapter 4 of Peter Tertzakian's book, " A Thousand Barrels a Second."

Chart 2. (Click on Image to Enlarge)

In conclusion, those Wall Street analysts with Harvard MBAs who are worried about a US economic slowdown causing a significant drop in year over year world oil demand will be surprised to find that such an occurrence will have very little affect on world incremental oil demand. Even if growth does slow one can still expect year over year U.S. oil consumption to increase in 2006 and 2007. Now is not a good time to sell quality oil company shares like ARD.

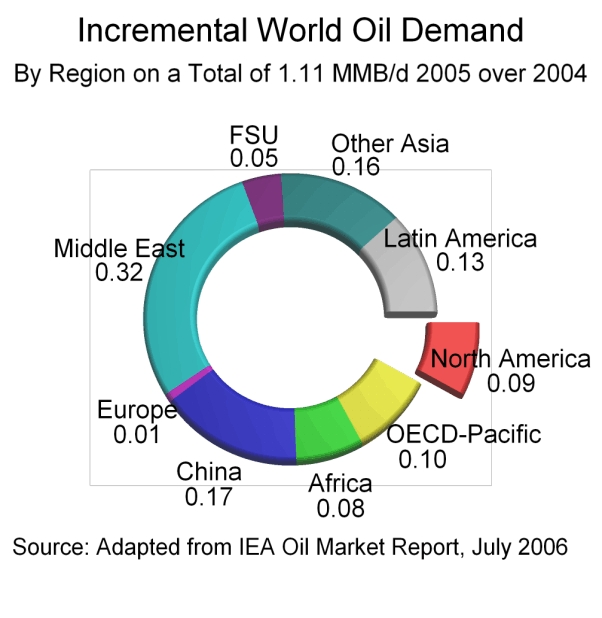

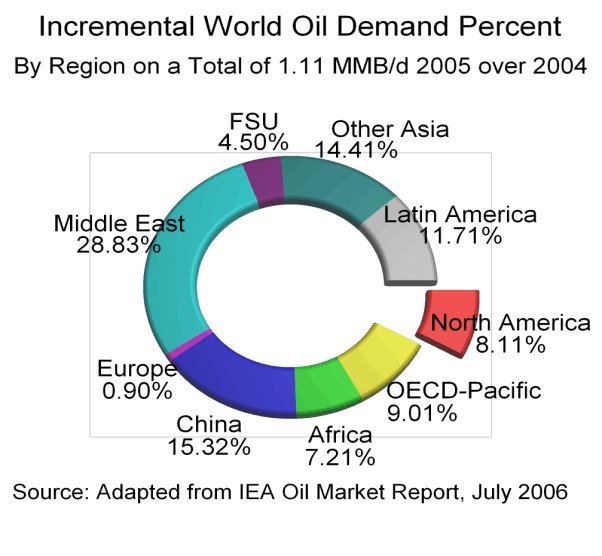

North American Incremental Oil Demand Accounted for only 8% of Total Between 2004 and 2005.

Between 2004 and 2005 world oil demand increased by 1.11 million barrels per day according to the International Energy Agency Oil Market Report dated July 2006. Of this incremental increase of 1.11 MMB/d demand in North America (USA and Canada) increased only 90,000 b/d as depicted in chart 1 below. In terms of percent this amount to just over 8% of the incremental world oil demand between 2004 and 2005 as depicted in chart 2 below.

Chart 1. (Click on Image to Enlarge)

Notice how the Middle East accounted for over 28% of the world incremental oil demand. This is nearly twice as much new demand as that of China between 2004 and 2005. With the new found oil wealth from rising oil prices the countries in the Middle East have vast amounts of money to spend on their economies. There is no doubt that the increase in GPD causes an increase in oil consumption. If you plot total Middle East GPD against total Middle East oil consumption you will see a line that increases against each axis. For more information on this phenomenon read chapter 4 of Peter Tertzakian's book, " A Thousand Barrels a Second."

Chart 2. (Click on Image to Enlarge)

In conclusion, those Wall Street analysts with Harvard MBAs who are worried about a US economic slowdown causing a significant drop in year over year world oil demand will be surprised to find that such an occurrence will have very little affect on world incremental oil demand. Even if growth does slow one can still expect year over year U.S. oil consumption to increase in 2006 and 2007. Now is not a good time to sell quality oil company shares like ARD.

posted by -Aztec- at 11:04 PM

![]()

{kind=link}