Arena Resources Announces Issuance of 1.15 Million Shares in Private Placement

Placement to Raise $30.2 million to Keep 100% of Credit Facility Available

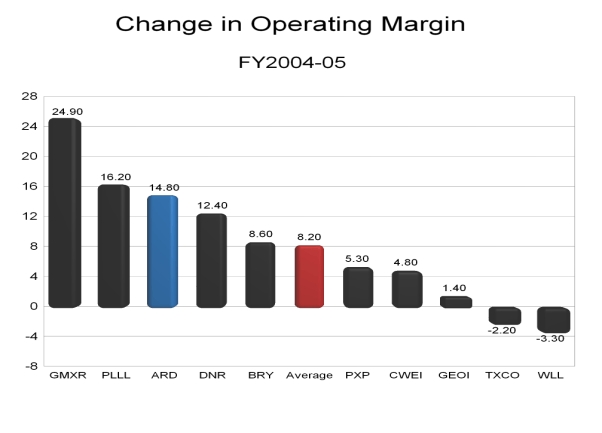

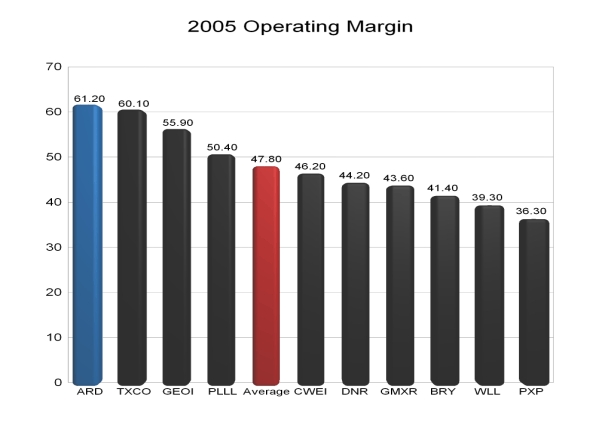

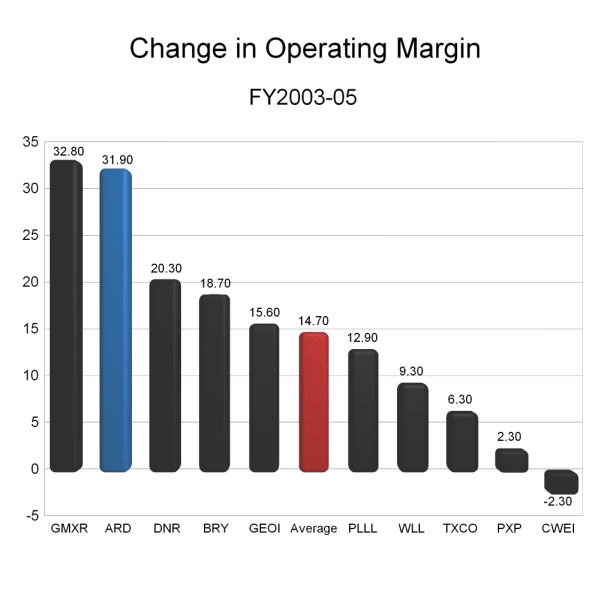

The Announcement is bullish. Historically ARD has used issuance of new shares to grow NAV 100% of the time. In other words, Oil Assets per Share have always increased even after the issuance of new shares. This has happened 100% of the time whenever ARD has issued new shares to raise cash.

Even if we account for the warrants being exercised in 2005 and 2006 that were connected with offerings in 2003 and 2004 the net result is the offerings still resulted in ARD being able to increase the oil assets per share.

Today's press release indicates ARD using the funds to, "...bridge the deficit between estimated 2006 cash flow and the company's current 2006 CAPEX budget of $65 million, and will allow the company to keep 100% of its credit facility available."

Keep in mind that just because ARD raised $30.2 million does not mean that they were expecting to have only $35 million in cash flow from operations. To the contrary, ARD will have cashflow from operations of about $65 million in 2006. The added $30.2 million will provide ARD with flexibility. Either they can boost their CapEx program in 2006 to $95.2 million or they can go out and purchase a property valued at $30.2 million or a combination of both while still allowing the company to, " keep 100% of its credit facility available." That is the key phrase.

I still believe there will be a major acquisition in 2006. Historically, whenever the credit facility and borrowing base are increased an acquisition has been soon to follow. Consider a portion of the transcript below taken from the May 11, 2006 first quarter conference call (scroll to 17:00 for the audio) :

John Lane (Lane Capital Markets): Hi Tim how are you?

Tim Rochford (ARD CEO): Good morning John how are you?

John Lane: Very Good.

Tim Rochford: Fine thankyou.

John Lane: Ahhh again, we all know of your ahh, Arena's desire to ahh acquire additional acreage but ahh I"d just like to congratulate you on your patience and in depth due diligence on you know on that acquisition front. Are there any prospects still coming to you that are worth considering or pretty much everything is priced you know in areas you're not willing to consider and are you probably content for the time being to still try to grow through expanding your current drilling on your existing properties?

Tim Rochford: Well that's a great question And one we are definitely on an aggressive mode in terms of looking and seeking out opportunities ahh but we're very cautious and and I can tell that Stan and I we just returned from the Permian Basin where we went out late last week and returned just a couple of days ago. We were there primarily to just look and evaluate projects. You know look kind of hands on and there's a number of deals that we are looking at but we have to be very cautious in this pricing environment right now. If you can't show, if we for our guidelines, if we can't show a component of of low risk probability ahh and potential that can evolve into the into the proved category we're not going to pay up for these properties. On the other hand, if we see that opportunity we're certainly postured and positioned financially to pull that trigger.

In conclusion, one should expect an acquisition to be announced in the near future. Considering that

1. Tim and Stan are,"definitely on an aggressive mode in terms of looking and seeking out opportunities" and that

2. there are a "number of deals" that they are "looking at" and

3. given the fact that they recently spent a few days in the Permian Basin to "look and evaluate projects" it is becoming very clear why the process of raising $30.2 million dollars has been accomplished: to "pull that trigger."

Everyone is led to believe by the press release that ARD is going to have cashflow from operations of $35 million and that the $30.2 million will close the gap to the $65 million CapEx budget for 2006. One should not assume that the gap between projected cashflow and the actual CapEx budget is $30.2 million. With 5 drilling rigs cashflow will easily be in excess of $65 million in 2006. (There is no gap.) The key is to focus on the second half of the sentence describing the purpose of this transaction: "allow the company to keep 100% of its credit facility available (after the purchase of a property.)" On the May 11th conference call Tim stated that, "...we're certainly postured and positioned financially..." On May 30th Shareholders witnessed Arena Resources CEO Tim Rochford, "...pull that trigger."

Placement to Raise $30.2 million to Keep 100% of Credit Facility Available

The Announcement is bullish. Historically ARD has used issuance of new shares to grow NAV 100% of the time. In other words, Oil Assets per Share have always increased even after the issuance of new shares. This has happened 100% of the time whenever ARD has issued new shares to raise cash.

Even if we account for the warrants being exercised in 2005 and 2006 that were connected with offerings in 2003 and 2004 the net result is the offerings still resulted in ARD being able to increase the oil assets per share.

Today's press release indicates ARD using the funds to, "...bridge the deficit between estimated 2006 cash flow and the company's current 2006 CAPEX budget of $65 million, and will allow the company to keep 100% of its credit facility available."

Keep in mind that just because ARD raised $30.2 million does not mean that they were expecting to have only $35 million in cash flow from operations. To the contrary, ARD will have cashflow from operations of about $65 million in 2006. The added $30.2 million will provide ARD with flexibility. Either they can boost their CapEx program in 2006 to $95.2 million or they can go out and purchase a property valued at $30.2 million or a combination of both while still allowing the company to, " keep 100% of its credit facility available." That is the key phrase.

I still believe there will be a major acquisition in 2006. Historically, whenever the credit facility and borrowing base are increased an acquisition has been soon to follow. Consider a portion of the transcript below taken from the May 11, 2006 first quarter conference call (scroll to 17:00 for the audio) :

John Lane (Lane Capital Markets): Hi Tim how are you?

Tim Rochford (ARD CEO): Good morning John how are you?

John Lane: Very Good.

Tim Rochford: Fine thankyou.

John Lane: Ahhh again, we all know of your ahh, Arena's desire to ahh acquire additional acreage but ahh I"d just like to congratulate you on your patience and in depth due diligence on you know on that acquisition front. Are there any prospects still coming to you that are worth considering or pretty much everything is priced you know in areas you're not willing to consider and are you probably content for the time being to still try to grow through expanding your current drilling on your existing properties?

Tim Rochford: Well that's a great question And one we are definitely on an aggressive mode in terms of looking and seeking out opportunities ahh but we're very cautious and and I can tell that Stan and I we just returned from the Permian Basin where we went out late last week and returned just a couple of days ago. We were there primarily to just look and evaluate projects. You know look kind of hands on and there's a number of deals that we are looking at but we have to be very cautious in this pricing environment right now. If you can't show, if we for our guidelines, if we can't show a component of of low risk probability ahh and potential that can evolve into the into the proved category we're not going to pay up for these properties. On the other hand, if we see that opportunity we're certainly postured and positioned financially to pull that trigger.

In conclusion, one should expect an acquisition to be announced in the near future. Considering that

1. Tim and Stan are,"definitely on an aggressive mode in terms of looking and seeking out opportunities" and that

2. there are a "number of deals" that they are "looking at" and

3. given the fact that they recently spent a few days in the Permian Basin to "look and evaluate projects" it is becoming very clear why the process of raising $30.2 million dollars has been accomplished: to "pull that trigger."

Everyone is led to believe by the press release that ARD is going to have cashflow from operations of $35 million and that the $30.2 million will close the gap to the $65 million CapEx budget for 2006. One should not assume that the gap between projected cashflow and the actual CapEx budget is $30.2 million. With 5 drilling rigs cashflow will easily be in excess of $65 million in 2006. (There is no gap.) The key is to focus on the second half of the sentence describing the purpose of this transaction: "allow the company to keep 100% of its credit facility available (after the purchase of a property.)" On the May 11th conference call Tim stated that, "...we're certainly postured and positioned financially..." On May 30th Shareholders witnessed Arena Resources CEO Tim Rochford, "...pull that trigger."

posted by -Aztec- at 7:18 AM

![]()

{kind=link}