Hello From Cabo San Lucas, Mexico

ARD higher at $33

ARD higher at $33

posted by -Aztec- at 10:19 AM

![]()

"The Biggest Little Oil and Gas Company on the Planet."

posted by -Aztec- at 10:01 PM

![]()

posted by -Aztec- at 7:41 AM

![]()

posted by -Aztec- at 7:55 AM

![]()

posted by -Aztec- at 2:57 PM

![]()

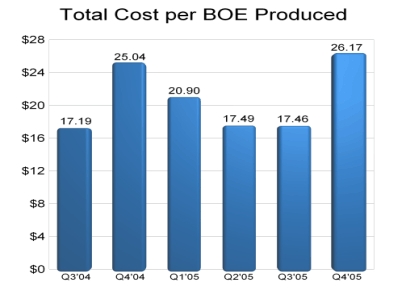

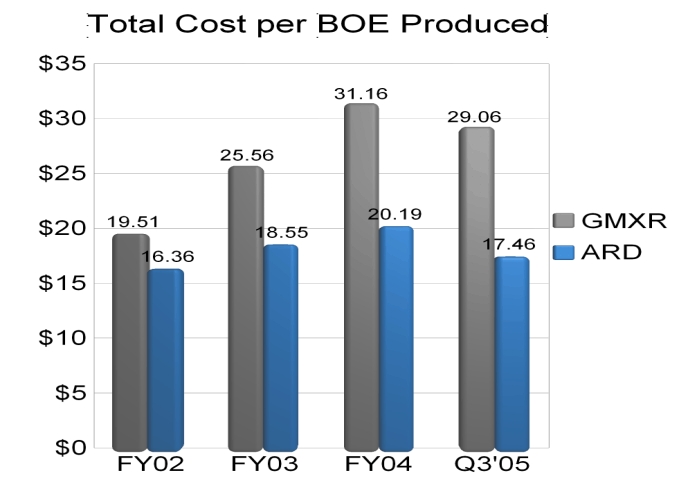

While some people are worried that ARD had a bad quarter I say relax! Not all metrics improve in a linear fashion every single quarter. Every company has challenges and Q4 seems to be a quarter in which ARD has the most challenges. One need only go back to Q4 2004. Take a look at the chart below? Does the rise in total cost per BOE produced look familiar? The numbers are amazingly familiar! Notice how Q4 in 2004 also saw a similar rise in total cost per BOE produced. This is nothing new. Take it in stride. If Q1 2005 is any indication as to what Q1 2006 will be like I think we can look forward to the total cost per BOE produced to decline next quarter and net margins to rise from current levels.

(Click on Image to Enlarge.)

Lets break down what I projected and what ARD actually came in at (2005 10K.)

Average Realized Price:

Estimate...$55

Actual.....$54.30

(I was off by 1.2%)

Revenue:

Estimate...$9.48mm

Actual.....$9.36mm

(I overestimated by 1.2%)

Net Margin:

Estimate...44%

Actual.....32%

(I overestimated by 27%)

Net Income:

Estimate...$4.07mm

Actual.....$3.01mm

(I overestimated by 26%)

Share Count:

Estimate...12.99mm

Actual.....13.09mm

(I underestimated by less than 1%)

All in all I nailed the:

1. Average realized price

2. Revenue

3. Share count

I was surprised and way off on my net margin...as was everyone else I"m sure. I have some theories on why I believe net margin came in 12 points below what I estimated:

1. Drilling program creates a lot of expense. These expenses are rising faster than the flow of oil from the wellheads. Hopefully in the future once production is established the LOE will decrease as infrastructure is already in place and paid for. I"m thinking that with all the new wells there will be more infrastructure requirements than most investors realize. I think Tim and Stan will mention something to this effect.

2. Possible delays in getting wells producing oil and connected to the system after the well has been drilled. Edadjootian mentioned that one of his concerns was ARD poking all the holes in the ground they want but just not being able to get them connected and producing in a timely manner. This may have something to do with the Q4 production being less than I anticipated.

3. Production declines greater than 6% yearly are being experienced in the oil patch in my estimation. This is one reason why I revised my 2006 Year end estimate from from something north of 2 million BOE to exactly 1 million BOE. If you take into account the greater than normal production declines in concert with the infrastructure intensive drilling program you have a recipe for lowered margins. I failed to take that into account and underestimated costs and thereby overestimating net margins. I"m hopeful that in the future when the infrastructure is in place that the production costs will be much lower thereby allowing net margins to again rise.

Was Q4 a complete failure? Absolutely not!

If you compare the Q4 YoY numbers ARD IMPROVED! For example, look at the 10K on page 72.

*Net margin increased from 29% to 32%

*Fully diluted EPS increased over 144%

*Revenues increased more than 215%

*Production increased YoY by 167% and QoQ by 22%. That is EXCELLENT folks!

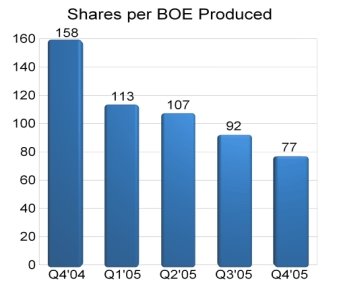

*Shares per BOE produced improved to 77.

(Shares per BOE produced is a metric that indicates how many shares of ARD you need to own in order to "own" 1 BOE of production.)

And even with our relative "disappointment" surrounding net margin...it was 32%. Not many companies can boast such a fat net margin. No doubt Q4 was a challenging quarter. However once we get the infrastructure in place, costs will decline and BOE produced will continue to rise. Historically Q4 has been a challenging quarter for the company. Last year Q4 production decreased QoQ. In Q3'04 production was 69,763. In Q4'04 production dropped to 64,494. So In light of the disappointment surrounding net margin in Q4'05 and higher than expected expenses I think it was a successful quarter. Keep in mind that Oil companies typically have a higher cost profile than NG companies...yet even in a challenging quarter such as this ARD was able to produce at a cost profile of $26.17 per BOE. This still beat GMXR with a cost profile of $28.69 per BOE produced.

posted by -Aztec- at 10:30 PM

![]()

posted by -Aztec- at 7:41 PM

![]()

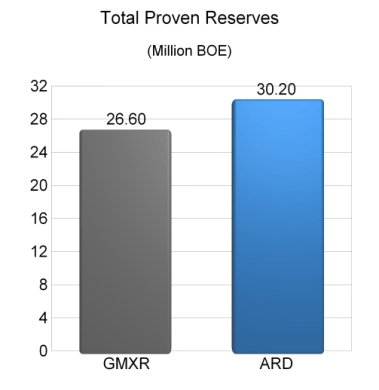

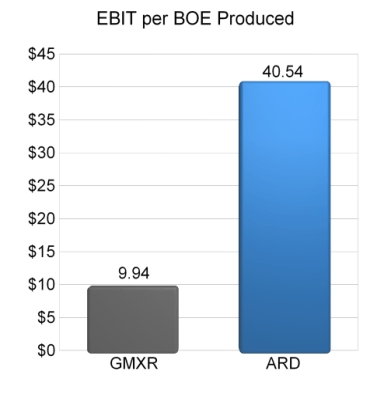

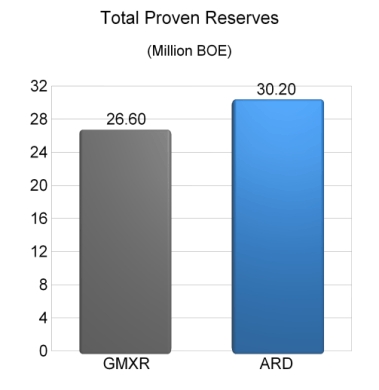

Based on the above proved reserve totals and the amount of EBIT per BOE produced we can determine the total amount of EBIT to be generated for each company.

The math is as follows:

GMXR:

26.6 mm BOE X $9.94 EBIT/BOE = $264.4 million.

(Lets round the $264.4 to $265 for easier math.)

ARD:

30.2 mm BOE X $40.54 EBIT/BOE = $1.224 BILLION.

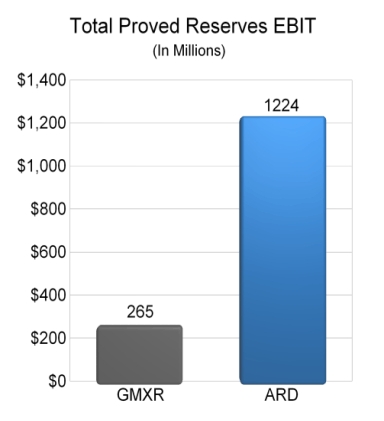

With the above facts of GMXR proved reserves capable of generating EBIT of $265 million and ARD proved reserves capable of generating EBIT of $1.224 billion it is clear that ARD is capable of producing over 4.6 X more EBIT than GMXR. The chart below shows the comparison of total proved reserves EBIT.

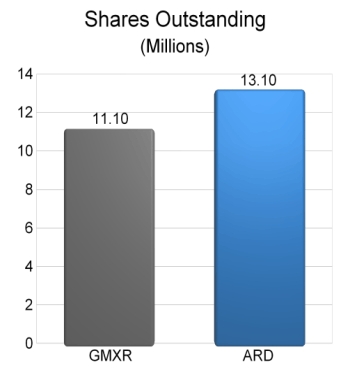

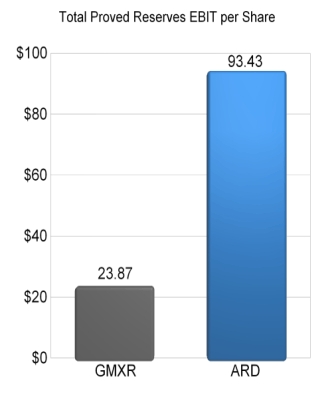

Now that we have the total EBIT that each proved reserve base is capable of producing we must now divide the amounts in the above chart by the total share count for each company to come up with the total EBIT per share.

The math looks like this:

GMXR: $265 million / 11.1 million = $23.87

ARD: $1.224 Billion/ 13.1 million = $93.43

The chart below compares the total proved reserves EBIT per share.

ARD is capable of generating over 3.9X more EBIT per share than GMXR ($93 to $23) even though GMXR has slightly more O&G assets per shares (2.39 to 2.3.) It should be crystal clear that the ARD reserves have much more value both in total and on a per share basis when compared to GMXR.

Based on GMXR current share price of $32.30 GMXR trades at over a 35% premium to the value of the EBIT per share based on the total proved reserves. Keep in mind that my 2006 target price on GMXR of $17 would put the share price below the proved reserve EBIT per share (40% discount to be exact) and would be a more realistic price and much closer to fair value.

In contrast, ARD current share price of $28.28 trades at a 230% discount to the EBIT per share based on total proved reserves. My 2006 price target on ARD of $60 would put ARD shares closer to a fair valuation and reduce the discount from 230% to a more reasonable 55% discount.

In summary it is easy to see that many investors are overestimating GMXR intrinsic value while at the same time grossly underestimating ARD intrinsic value. Valuing both GMXR and ARD reserves based on the amount of profit derived from each BOE and the actual number of BOE proved reserves per share it is easy to see that ARD shares have a much higher intrinsic value. This is a primary reason why ARD shares deserve to have a valuation that not only exceeds that of GMXR but exceeds that of GMXR by a wide margin. Even if GMXR proved reserves were doubled, ARD would still have more total proved reserves EBIT as well as proved reserves EBIT per share. Look for ARD share valuation to surpass that of GMXR in 2006 as the market begins to takes notice of these facts.

posted by -Aztec- at 12:26 PM

![]()

posted by -Aztec- at 11:57 AM

![]()

End Transcript...

*CFO Ken Kenworthy Sr. *

Did you hear what KEN mumbled at the end? The part that he mumbled should have been the part that was annunciated with clarity and emphasis. Instead he tried to do the old mumbling trick...trying to slip a zinger in under the radar of the listeners. That just happened to be one of the most important statements in the entire conference call that listeners NEEDED to latch onto. With that said it should come as no surprise that if NG goes lower GMXR will be unable to go forward with their drilling program. That is how close to the edge they are driving this company. They are being RECKLESS with the company. There is very little margin of error for the company or shareholders. I have been table pounding all along that GMXR of all companies should NOT be taking such an aggressive stand in the 2006 CAPEX program given the fact that their revenue per BOE produced is worth $39 based on $6.50 NG. Also with their costs up over $29.06 there is only a margin of $9.94 per BOE produced. That is razor thin folks. If NG drops to say $5.00 per Mcfe then each GMXR BOE will only be worth $30. With rising costs for drilling, workers, etc I see the costs of $29.06 per BOE produced rising above $30. With that said GMXR is facing NG production at a loss! If you have your heart set on owning NG then I would highly recommend you think about a low cost producer like UPL. They can be profitable with NG prices under $2.75.

GMXR is very near a cliff right now. The reserves in the ground won't be able to prevent an early collapse of share price or market cap if NG prices should go any lower. Keep in mind that my $17 fair value assumes NG prices of $6.50. If NG prices would sink lower than $6.50 per mcfe then a share price of $17 would be unsustainable. Production at a loss would bring early selling to GMXR shares and my target price of $17 would be reached sooner than anticipated.

posted by -Aztec- at 2:58 PM

![]()

posted by -Aztec- at 10:33 PM

![]()

posted by -Aztec- at 12:02 AM

![]()

{kind=link}

{kind=link}