Can Saudi Arabia Expect to Top Record Oil Exports of 1980?Geology of Oil Fields and Saudi Population Growth may Make such a Feat ImpossibleSaudi Arabia is the world's largest producer of crude oil. In 2005 Saudi oil production was estimated at 9.3 million barrels/day (b/d.) Based on total worldwide production (84.3 million b/d) Saudi production accounted for 11%. Since Saudi Arabia is the world's largest producer of oil it is only logical that their production, consumption, and exports should be under the microscope and closely watched.

In his book, "Twilight in the Desert," Matthew Simmons pieced together the evidence that indicates major problems with Saudi Arabia's major oil fields and specifically the world's largest: Ghawar. Many of the problems originate with the fact that the largest oil fields were discovered first. Hence they are the oldest. Elderly oil fields tend to have 'health problems' just like elderly people do. In the case of old oil fields the major problem is declining production. Certainly there are steps that are taken to treat the 'symptoms' of declining oil production. Over time maintaining (let alone increasing) production becomes very challenging.

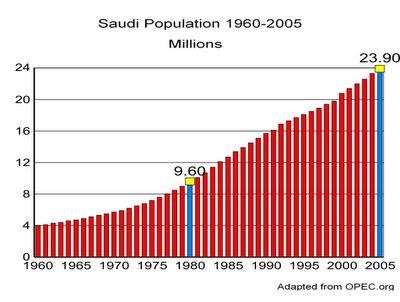

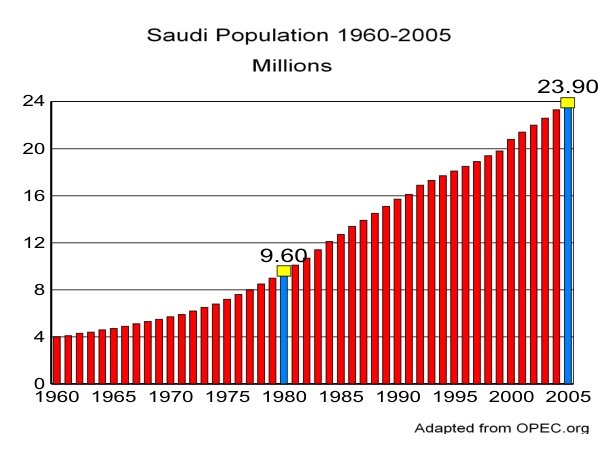

While many focus on the problems associated with the Saudi Oil fields one must not discount the problems created by Saudi Arabia's increasing population. Saudi Arabia is a country with a rapidly expanding population. Between 2000 and 2005 the Saudi population increased by an average of over 600,000 people each year. The chart below depicts yearly estimated Saudi population between 1960 and 2005.

(Chart 1)

(click on image to enlarge)

The chart above depicting

Saudi population (Chart 1) indicates that the population was 9.6 million people in 1980 and 23.9 million people in 2005. In other words the population was just about 2.5 times larger in 2005 than in 1980. This change took place in a span of 25 years. With a growing population it is only evident that the Saudi society will have larger oil requirements. Chart 2 below depicts

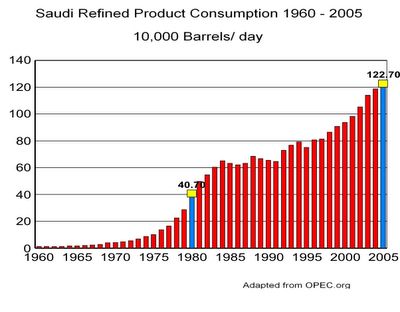

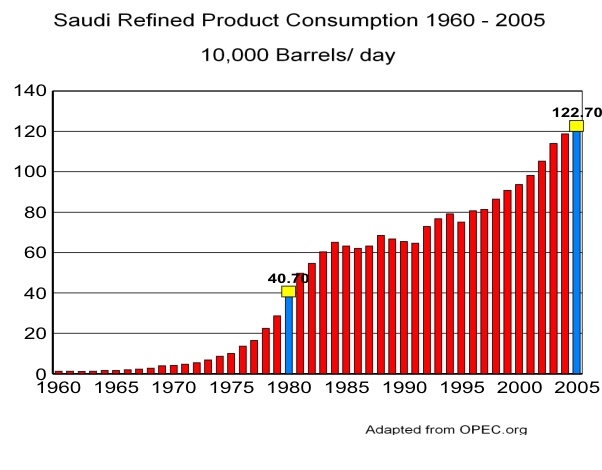

Saudi refined product consumption between 1960 and 2005.

(Chart 2)

(click on image to enlarge)

Again if we take a look at 1980 it is noted that the refined product consumption was 407,000 b/d as noted in chart 2 above. In 2005 internal consumption increased to 1,227,000 b/d. During the 25 year span between 1980 and 2005 Saudi refined product consumption more than tripled.

Based on this fact it should be extremely evident that Saudi oil exports will be limited not only by the geological problems associated with production but also with the country's internal thirst for oil consumption.

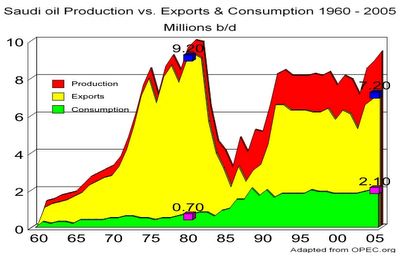

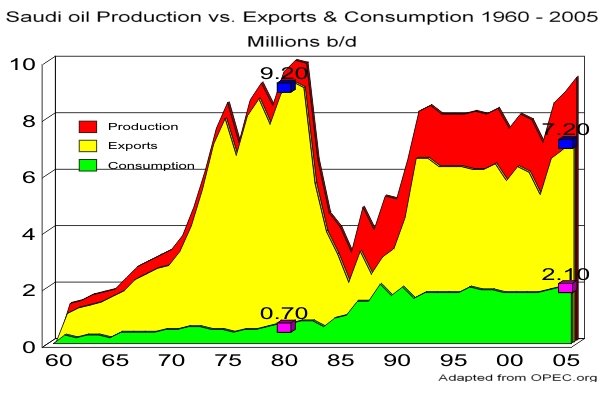

The chart below (chart 3) highlights Saudi oil production, exports and consumption between 1960 and 2005. The red area indicates Saudi production each year in terms of millions b/d. Saudi Arabia's best year was 1980 when they produced an average of 9.9 million b/d. Fast forward 25 years and they were only able to produce 9.3 million b/d. Keep in mind that production is depicted in the red area. In order to match 1980's production level Saudi Arabia would have to increase production by about 600,000 b/d or 6.4%.

Due to population growth we already discussed how Saudi Arabia has increased demand for oil productions as depicted in chart 2 above. In chart 3 below we have determined the amount of oil Saudi Arabia produces and then consumes (demand and/or storage) simply by subtracting published

exports from published

production figures. The amount of Saudi production that is used within the country is depicted with the green area. In 1980 Saudi Arabia kept 1 out of every 14.1 barrels of oil produced for internal consumption (7.0%). In 2005 Saudi Arabia kept 1 out of every 4.4 barrels produced (22.6%). The pink squares denotes 1980 consumption of 700,000 b/d and 2005 consumption of 2.1 million b/d.

Not only does Saudi Arabia have to find ways to replace production that is lost to geological natural decline in the oil fields but in order to maintain their exports at 1980 levels they must now produce an extra 1.4 million b/d to account for the increase in Saudi oil demand caused in large part to the growth of the Saudi population. One can certainly count on the population to continue growing along with their demand for oil.

(Chart 3)

(click on image to enlarge)

Saudi Oil ExportsThe yellow shaded area in chart 3 above indicates the oil that was actually exported. In 1980 total exports amounted to 9.2 million b/d. In 2005 total exports came in at 7.2 million b/d. What caused exports to decline? Actual production declined by 600,000 b/d. Internal consumption of oil increased by 1.4 million b/d. If we add these amounts up we come up with 2 million b/d in reduced oil exports. 2005 Exports would have to be increased 27.7% to match 1980 exports.

In order to export 9.2 million b/d as was done in 1980 and to satisfy the oil needs of the Saudi population in 2005 (2.1 million b/d) total production would have to equal 11.3 million b/d. Given the fact that estimated 2005 Saudi

production was 9.3 million b/d we would need to see an increase of 2 million b/d (21.5%) from 2005 levels.

In conclusion, given the fact that Saudi Arabia has serious problems with their oil fields of which most notable is the Ghawar (world's largest oil field) along with Saudi Arabia's growing growing thirst for oil it should come as no surprise that the chances of Saudi Arabia ever matching the level of exports in 1980 is extremely doubtful.

{kind=link}