ARD v GMXR Part II

How OVERVALUED is GMXR?

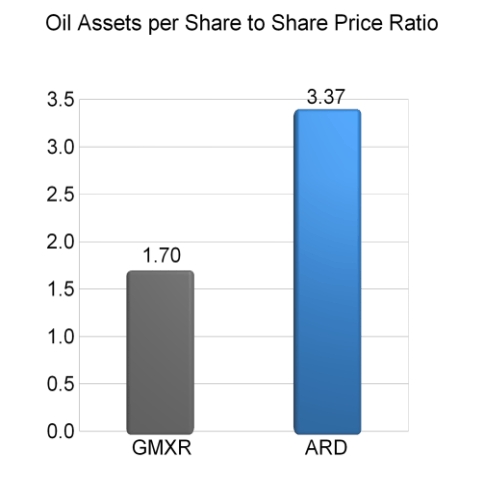

Lets compare Oil Assets per Share between ARD and GMXR. Based on P1 (that is the most important "P" and since ARD's P2 is unpublished we will refrain from bringing P2 into the equasion) the following Oil Assets per Share should be noted:

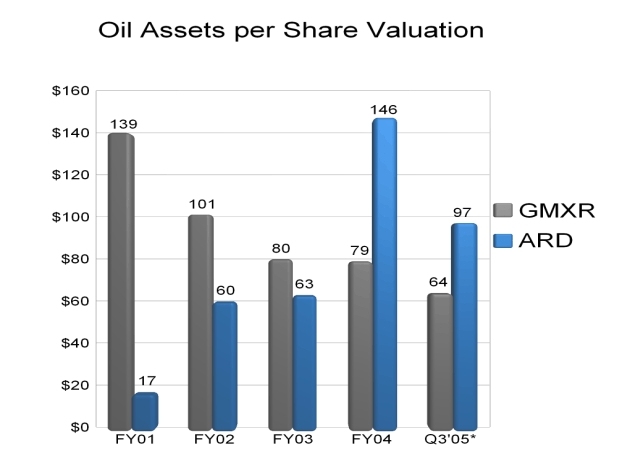

ARD.........1.62 BOE

GMXR........1.07 BOE

(Click on image to enlarge.)

I have stated in the past that if ARD were priced based on GMXR valuation ARD would be higher on a per share basis since ARD has more OAPS (Oil Assets per Share) and more production per share than GMXR. Obviously Mr.Market has the GMXR v ARD share price way out of whack by pricing GMXR higher than ARD. I realize there are other factors driving GMXR higher.

For now lets hold off on that discussion. Lets keep our focus squarely on ARD v GMXR valuation. Lets do something a little different. Instead of pricing ARD based on GMXR valuation lets price GMXR based on ARD valuation and we all know that pricing GMXR based on ARD would be OVERPRICING GMXR as ARD is the better franchise. But for a minute let's assume that the GMXR franchise is every bit as good as ARD's. Lets price out GMXR based on OAPS:

ARD.........1.62 BOE

GMXR.......1.07 BOE

If you divide 1.07 by 1.62 you get the quotient of 0.66. Put another way, based on OAPS GMXR shares should be priced at 66% of ARD current share price. So if ARD currently trades at $27.45 then GMXR should trade at $18.11. The math is like this:

$27.45 X 0.66 = $18.11

Pricing GMXR based on Production

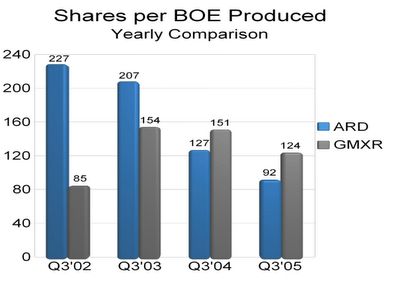

Now if you want to price GMXR based on ARD production then we should take a look at shares per BOE produced:

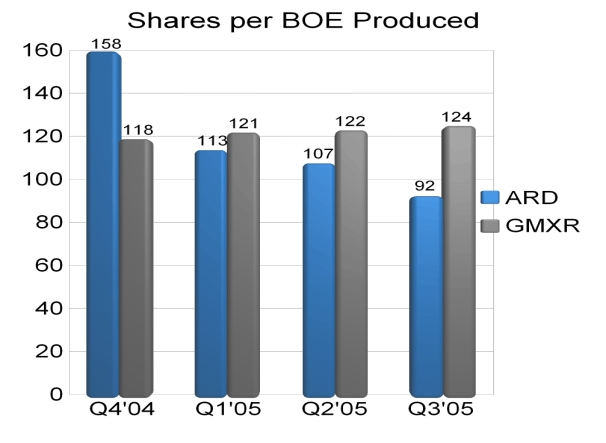

ARD........92

GMXR......124

(Click on image to enlarge.)

Shares per BOE produced simply means you would have to go out and purchase 92 shares of ARD or 124 shares of GMXR in order to "own" 1 BOE of production. Based on current ARD share price of $27.45 it would cost $2,525 to "own" 1 BOE of ARD production. Based on current GMXR share price of $35.33 it would cost $4,380 to "own" 1 BOE of GMXR production. How do we figure out what GMXR should be worth based on production when comparing it to ARD? Since it costs $2,525 to "own" 1 BOE of ARD production lets also assume that it should cost the same to "own" that 1 BOE of GMXR production. In other words we must divide the total cost of $2,525 by 124 (GMXR shares per BOE produced) to arrive at $20.36. If each GMXR share were valued at $20.36 and it takes 124 GMXR shares to "own" 1 BOE of production the math looks like this:

$20.36 X 124 = $2,525

$2,525 is what it would cost to "own" 1 BOE of ARD and based on that cost it would take a GMXR share price of $20.36 to be in line with ARD. However we all know that ARD outproduces GMXR in terms of production growth and absolute production. So to say that GMXR should be valued on par with ARD is wrong. GMXR should be valued less than that of ARD.

The Advantage of Selling GMXR and Buying ARD

I'd like to clarify that I do not believe the wheels are coming off the cart at GMXR. What I am saying is that in relation to ARD the GMXR shares are grossly overpriced. Either that or ARD shares are grossly underpriced. In any case there is a major valuation imbalance between ARD and GMXR 'currency.' What is so unusual about the imbalance is that it favors the inferior company: GMXR.

So in a nutshell, not only is GMXR overpriced in terms of oil assets per share but it is also overpriced in terms of production per share. Closer examination reveals that based on OAPS GMXR deserves a share price of $18 based on ARD valuation of OAPS. Also if you price GMXR shares based on ARD production per share then each GMXR share is only worth $20. Keep in mind that this would assume that GMXR has the SUPERIOR franchise of ARD. Since it does NOT have the superior franchise of ARD it deserves to be valued LOWER than $18 (OAPS) or $20 (production.)

ARD provides both a superior franchise AND value. (Read the blog and/or do a little D&D.)

GMXR provides NEITHER.

GMXR is an AVERAGE to SUBPAR company with AVERAGE to SUBPAR management and an AVERAGE TO SUBPAR cost structure. In relation to the superior franchise ARD, GMXR is overpriced and thus there is NO value. In other words, GMXR is priced ABOVE fair value.

If I did own the GMXR shares I"d be exchanging them for ARD shares today as ARD is not only a better company from top to bottom but the shares are more attractively priced. By exchanging 1000 GMXR shares @ $36.42 for ARD shares priced @ $27.66 you would get:

1,316 ARD shares.

Effectively your ownership of oil assets would jump from 1,070 BOE (based on 1000 shares of GMXR) to 2,131 BOE (based on 1,316 shares of ARD.) I would jump at the opportunity to sell an average to subpar oil company for a superior oil company while at the same time increase my ownership of oil assets by 99% (from 1,070 BOE to 2,131 BOE.)

In terms of production you would go from owning 8.06 BOE of production (1000 / 124) to owning 14.30 BOE of production. (1,316 / 92.) This represents an increase in production 'ownership' of 77%.

The choice is EXTREMELY SIMPLE AND CLEAR.

This is why I blog about it: I want others to profit from the rise in GMXR share and take advantage of the opportunity with ARD. I want you GMXR shareholders to get the ARD shares before the arrogant Wallstreet pinheads do. I know for a fact that institutional investors view retail investors as idiots. Those of you retail investors that are not idiots should be offended and take action.

In conclusion, it is easy to see that based on ARD's superior Oil Assets per Share and production either GMXR share price of $35.90 has a long way to fall or ARD share price of $27.50 has a long way to rise. Make no mistake about it, the gap in share price between GMXR and ARD will close and eventually ARD share price will exceed that of GMXR. GMXR shareholders would be prudent to study the advantages of trading in their GMXR shares for those of ARD.

How OVERVALUED is GMXR?

Lets compare Oil Assets per Share between ARD and GMXR. Based on P1 (that is the most important "P" and since ARD's P2 is unpublished we will refrain from bringing P2 into the equasion) the following Oil Assets per Share should be noted:

ARD.........1.62 BOE

GMXR........1.07 BOE

%20ARD%20v%20GMXR.jpg)

(Click on image to enlarge.)

I have stated in the past that if ARD were priced based on GMXR valuation ARD would be higher on a per share basis since ARD has more OAPS (Oil Assets per Share) and more production per share than GMXR. Obviously Mr.Market has the GMXR v ARD share price way out of whack by pricing GMXR higher than ARD. I realize there are other factors driving GMXR higher.

For now lets hold off on that discussion. Lets keep our focus squarely on ARD v GMXR valuation. Lets do something a little different. Instead of pricing ARD based on GMXR valuation lets price GMXR based on ARD valuation and we all know that pricing GMXR based on ARD would be OVERPRICING GMXR as ARD is the better franchise. But for a minute let's assume that the GMXR franchise is every bit as good as ARD's. Lets price out GMXR based on OAPS:

ARD.........1.62 BOE

GMXR.......1.07 BOE

If you divide 1.07 by 1.62 you get the quotient of 0.66. Put another way, based on OAPS GMXR shares should be priced at 66% of ARD current share price. So if ARD currently trades at $27.45 then GMXR should trade at $18.11. The math is like this:

$27.45 X 0.66 = $18.11

Pricing GMXR based on Production

Now if you want to price GMXR based on ARD production then we should take a look at shares per BOE produced:

ARD........92

GMXR......124

.jpg)

(Click on image to enlarge.)

Shares per BOE produced simply means you would have to go out and purchase 92 shares of ARD or 124 shares of GMXR in order to "own" 1 BOE of production. Based on current ARD share price of $27.45 it would cost $2,525 to "own" 1 BOE of ARD production. Based on current GMXR share price of $35.33 it would cost $4,380 to "own" 1 BOE of GMXR production. How do we figure out what GMXR should be worth based on production when comparing it to ARD? Since it costs $2,525 to "own" 1 BOE of ARD production lets also assume that it should cost the same to "own" that 1 BOE of GMXR production. In other words we must divide the total cost of $2,525 by 124 (GMXR shares per BOE produced) to arrive at $20.36. If each GMXR share were valued at $20.36 and it takes 124 GMXR shares to "own" 1 BOE of production the math looks like this:

$20.36 X 124 = $2,525

$2,525 is what it would cost to "own" 1 BOE of ARD and based on that cost it would take a GMXR share price of $20.36 to be in line with ARD. However we all know that ARD outproduces GMXR in terms of production growth and absolute production. So to say that GMXR should be valued on par with ARD is wrong. GMXR should be valued less than that of ARD.

The Advantage of Selling GMXR and Buying ARD

I'd like to clarify that I do not believe the wheels are coming off the cart at GMXR. What I am saying is that in relation to ARD the GMXR shares are grossly overpriced. Either that or ARD shares are grossly underpriced. In any case there is a major valuation imbalance between ARD and GMXR 'currency.' What is so unusual about the imbalance is that it favors the inferior company: GMXR.

So in a nutshell, not only is GMXR overpriced in terms of oil assets per share but it is also overpriced in terms of production per share. Closer examination reveals that based on OAPS GMXR deserves a share price of $18 based on ARD valuation of OAPS. Also if you price GMXR shares based on ARD production per share then each GMXR share is only worth $20. Keep in mind that this would assume that GMXR has the SUPERIOR franchise of ARD. Since it does NOT have the superior franchise of ARD it deserves to be valued LOWER than $18 (OAPS) or $20 (production.)

ARD provides both a superior franchise AND value. (Read the blog and/or do a little D&D.)

GMXR provides NEITHER.

GMXR is an AVERAGE to SUBPAR company with AVERAGE to SUBPAR management and an AVERAGE TO SUBPAR cost structure. In relation to the superior franchise ARD, GMXR is overpriced and thus there is NO value. In other words, GMXR is priced ABOVE fair value.

If I did own the GMXR shares I"d be exchanging them for ARD shares today as ARD is not only a better company from top to bottom but the shares are more attractively priced. By exchanging 1000 GMXR shares @ $36.42 for ARD shares priced @ $27.66 you would get:

1,316 ARD shares.

Effectively your ownership of oil assets would jump from 1,070 BOE (based on 1000 shares of GMXR) to 2,131 BOE (based on 1,316 shares of ARD.) I would jump at the opportunity to sell an average to subpar oil company for a superior oil company while at the same time increase my ownership of oil assets by 99% (from 1,070 BOE to 2,131 BOE.)

In terms of production you would go from owning 8.06 BOE of production (1000 / 124) to owning 14.30 BOE of production. (1,316 / 92.) This represents an increase in production 'ownership' of 77%.

The choice is EXTREMELY SIMPLE AND CLEAR.

This is why I blog about it: I want others to profit from the rise in GMXR share and take advantage of the opportunity with ARD. I want you GMXR shareholders to get the ARD shares before the arrogant Wallstreet pinheads do. I know for a fact that institutional investors view retail investors as idiots. Those of you retail investors that are not idiots should be offended and take action.

In conclusion, it is easy to see that based on ARD's superior Oil Assets per Share and production either GMXR share price of $35.90 has a long way to fall or ARD share price of $27.50 has a long way to rise. Make no mistake about it, the gap in share price between GMXR and ARD will close and eventually ARD share price will exceed that of GMXR. GMXR shareholders would be prudent to study the advantages of trading in their GMXR shares for those of ARD.

posted by -Aztec- at 8:41 AM

![]()

%20ARD%20v%20GMXR.jpg)

{kind=link}