ARD v WGR: Valuation

Folks,WGR (Western Gas Resources) was one of the two companies with an offer to be bought out by Anadarko.

I had some questions about WGR, the potential transaction and the implications with ARD. Here are some of my questions:

1. What did Anadarko value the proved reserves of WGR at?

2. What are the WGR proved reserves per share?

3. What is the valuation of these proved reserves per share based on Friday's closing price of $6.41 NG and $70.87 CL?

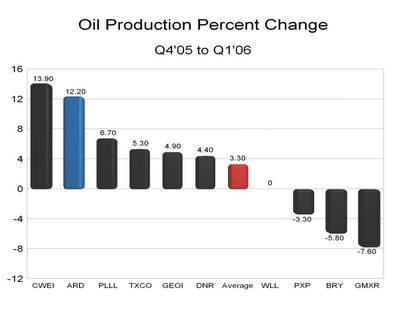

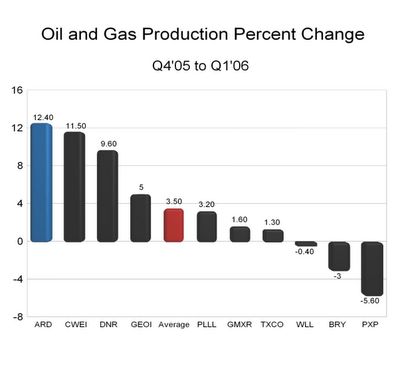

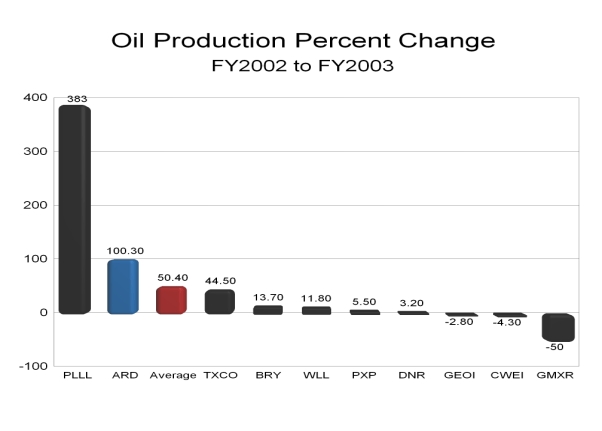

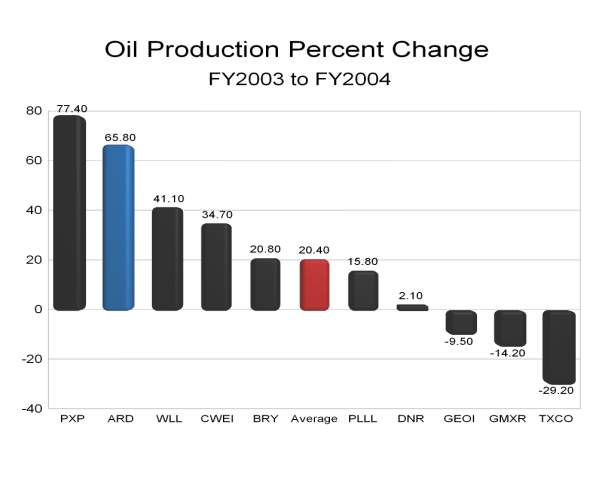

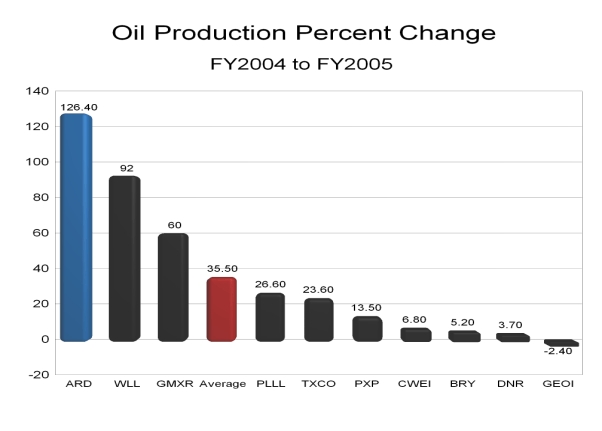

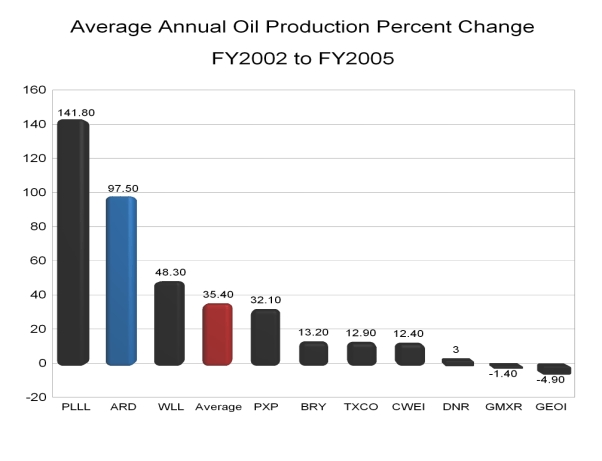

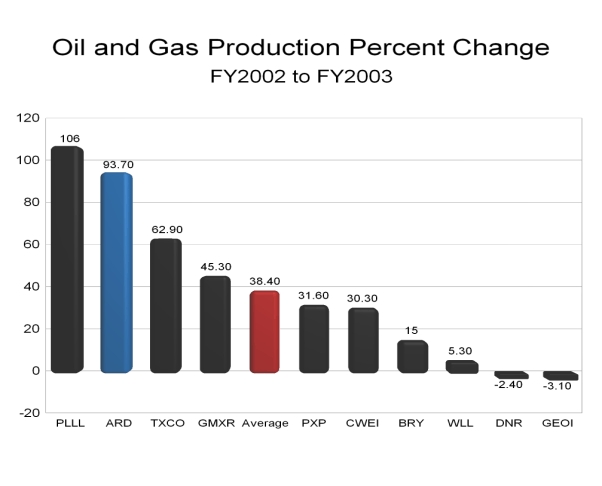

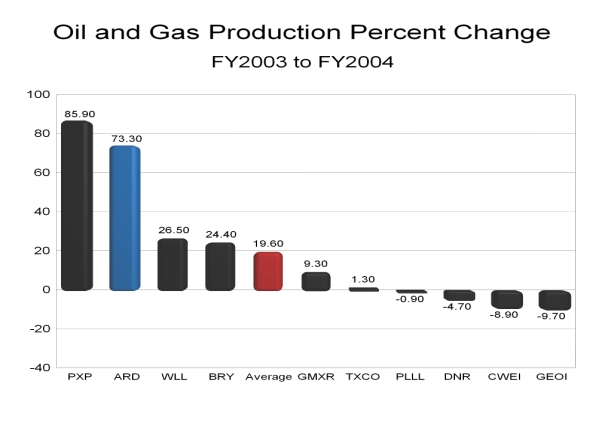

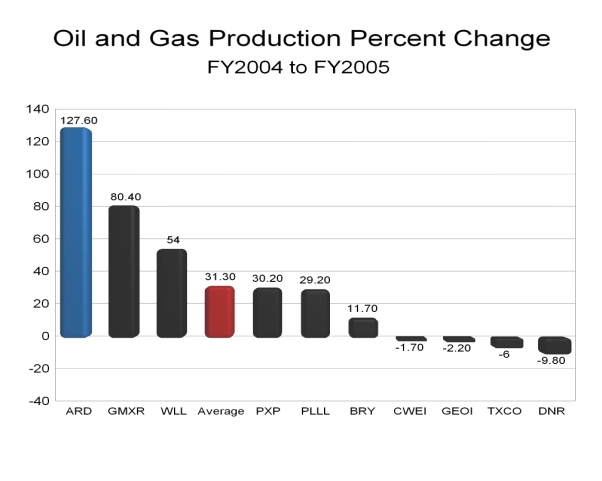

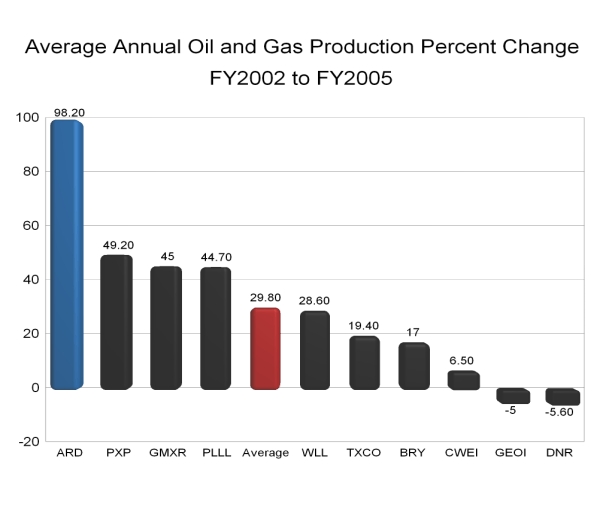

4. What are the historical trends of WGR oil and gas production?

5. How does this production growth compare to ARD?

6. What are the historical trends of WGR oil and gas proved reserves?

7. How does this proved reserves growth compare to ARD?

8. What are the historical trends in proved reserves per share for both WGR and ARD?

These are only a sampling of the questions that I had. I did an initial investigation to determine production, proved reserves, proved reserves per share and valuation of proved reserves per share for 2003, 2004, 2005 for WGR.

My findings will blow ARD shareholders away. It will take me time to do the data mining, construct the charts, compose my thoughts and present my analysis. (Hopefully I can have this Analysis posted on the ARD blog in the coming weeks.)

For starters lets just say this:

Year End 2005 Proved Reserves Value per Share:

WGR.......$81.04

ARD......$148.44

Current Share Price:

WGR.......$59.67

ARD.......$31.70

Certainly these two facts alone don't mean much. When my analysis is posted I hope to build a case with strong supporting evidence that ARD shares are more valuable than WGR shares and that based on current prices ARD shareholders have tremendous upside potential. Please keep in mind my 2006 price target for ARD has been $60 since February 1, 2006.

The case will be made that ARD is the superior company, has the higher intrinsic value per share while at the same time trading at only 53% of the markets valuation of WGR shares. Buckle up folks. ARD shares will be volatile. They are headed higher. Much higher. The fact that a company (Anadarko) wants to buy another company (WGR) that has less value per share than ARD but at an 88% premium to ARD shares speaks volumes of where ARD shares are headed and the magnitude of the move to come.

What makes this comparison so compelling is the fact that it isn't simply an irrational stock market pricing WGR at $59.67. Rather it is an offer from Anadarko to buy out WGR at a price that is even higher than $59.67. Even if Anadarko's offer to buyout WGR is irrational it raises the stakes and ups the ante on valuation of proved reserves per share and ultimately share price. Even if one would assume that Anadarko's offer IS IRRATIONAL it is EVEN MORE IRRATIONAL that ARD shares trade at such a discount to WGR in light of the fact that ARD has higher intrinsic value per share and superior fundamentals to that of WGR.

Folks,WGR (Western Gas Resources) was one of the two companies with an offer to be bought out by Anadarko.

I had some questions about WGR, the potential transaction and the implications with ARD. Here are some of my questions:

1. What did Anadarko value the proved reserves of WGR at?

2. What are the WGR proved reserves per share?

3. What is the valuation of these proved reserves per share based on Friday's closing price of $6.41 NG and $70.87 CL?

4. What are the historical trends of WGR oil and gas production?

5. How does this production growth compare to ARD?

6. What are the historical trends of WGR oil and gas proved reserves?

7. How does this proved reserves growth compare to ARD?

8. What are the historical trends in proved reserves per share for both WGR and ARD?

These are only a sampling of the questions that I had. I did an initial investigation to determine production, proved reserves, proved reserves per share and valuation of proved reserves per share for 2003, 2004, 2005 for WGR.

My findings will blow ARD shareholders away. It will take me time to do the data mining, construct the charts, compose my thoughts and present my analysis. (Hopefully I can have this Analysis posted on the ARD blog in the coming weeks.)

For starters lets just say this:

Year End 2005 Proved Reserves Value per Share:

WGR.......$81.04

ARD......$148.44

Current Share Price:

WGR.......$59.67

ARD.......$31.70

Certainly these two facts alone don't mean much. When my analysis is posted I hope to build a case with strong supporting evidence that ARD shares are more valuable than WGR shares and that based on current prices ARD shareholders have tremendous upside potential. Please keep in mind my 2006 price target for ARD has been $60 since February 1, 2006.

The case will be made that ARD is the superior company, has the higher intrinsic value per share while at the same time trading at only 53% of the markets valuation of WGR shares. Buckle up folks. ARD shares will be volatile. They are headed higher. Much higher. The fact that a company (Anadarko) wants to buy another company (WGR) that has less value per share than ARD but at an 88% premium to ARD shares speaks volumes of where ARD shares are headed and the magnitude of the move to come.

What makes this comparison so compelling is the fact that it isn't simply an irrational stock market pricing WGR at $59.67. Rather it is an offer from Anadarko to buy out WGR at a price that is even higher than $59.67. Even if Anadarko's offer to buyout WGR is irrational it raises the stakes and ups the ante on valuation of proved reserves per share and ultimately share price. Even if one would assume that Anadarko's offer IS IRRATIONAL it is EVEN MORE IRRATIONAL that ARD shares trade at such a discount to WGR in light of the fact that ARD has higher intrinsic value per share and superior fundamentals to that of WGR.

posted by -Aztec- at 2:36 PM

![]()

{kind=link}